We have been walking in the dark for several weeks. While the market tried to guess where the pandemic would lead the economy, we barely received any data to confirm or deny our hypothesis. We knew jobless claims would skyrocket but that doesn’t tell us how many real jobs will be lost.

As we move forward with the second earnings season of the year, CEO’s comments on their businesses will be crucial in our decision-making process. Remember: power is knowledge.

Let’s look at two companies that have seen their stock prices plummet since the beginning of the year. Those are obviously riskier plays, but those risks could come with great rewards down the road.

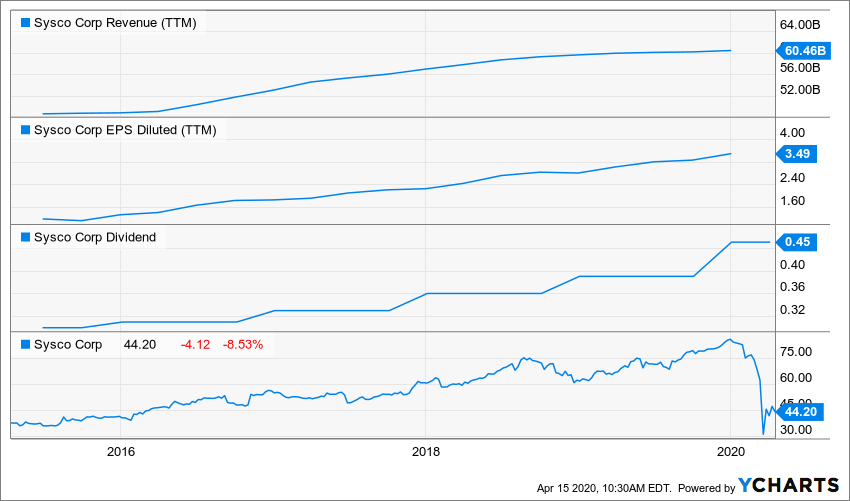

SYSCO (SYY) -36%

Business Model

Sysco is the largest U.S. foodservice distributor, boasting 16% market share of the highly fragmented foodservice distribution industry. Sysco distributes over 400,000 food and non-food products to restaurants (62% of revenue), healthcare facilities (8%), travel, leisure, and retail (9%), education and government buildings (9%), and other locations (12%) where individuals consume away-from-home meals. In 2018, 80% of the firm’s revenue was U.S.-based, with 8% from Canada, 5% from the U.K., 3% from France, and 4% other.

The Company in a Nutshell

- Sysco dominates the food distribution on U.S. soil, it remains a highly fragmented industry.

- Management is investing in local markets to grow its business.

- Sysco shows more than twice the sales of the second largest food distributor (US Foods).

What could go wrong?

What’s wrong with a food distribution service? Is it not the kind of business that should thrive right now? Not if your business delivers food to restaurants (62% of revenue) and travel and leisure businesses (9%). You can expect a very poor year for this company as most analysts expect double-digit revenue declines. You may want to wait until you read their latest quarterly update before making a move.

What could go right?

While the short-term picture is quite dim, the SYY business model remains solid. The company was doing very well prior to the COVID-19. The company should get out of this crisis stronger than its competitors due to its size and scale. The food distribution market is highly fragmented, and this will be a perfect situation for this soon-to-be dividend king to grab additional market share.

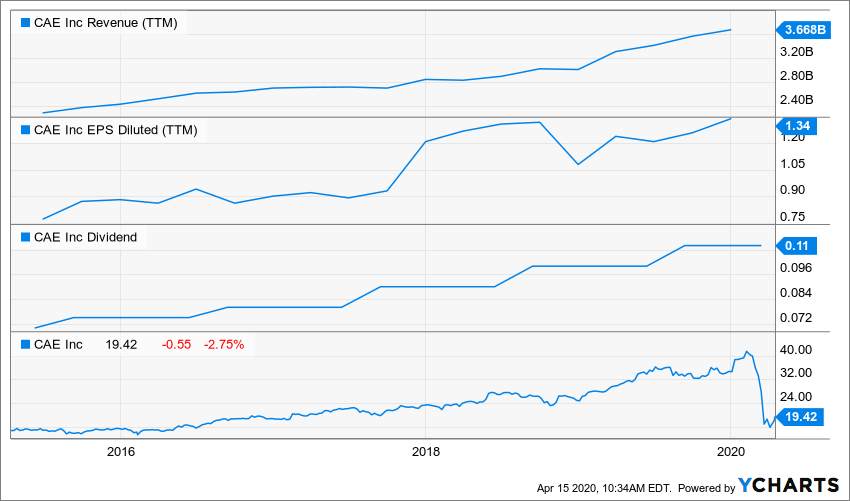

CAE (CAE) -43%

Business Model

CAE Inc is a global company focused on delivering training for the civil aviation, defense, security, and healthcare markets. Multiple types of simulators and synthetic exercises may be sold to customers to serve as alternatives for live-training experiences. The company’s training solutions are provided through products and services. CAE has many different training locations where clients can be trained and educated through a series of programs. Additionally, part of its revenues come from supplying aviation personnel on a lease, along with providing aviation support organizations. Roughly one-third of sales are from the United States, with the remainder split among several other nations.

The Company in a Nutshell

- Throughout the years, CAE has developed a well-diversified business.

- CAE’s revenue comes from 60% services and 40% products.

- 36% of its revenues are coming from the US, 27% from Europe and 36% from other countries.

What could go wrong?

This is a first: a company that not only cut its dividend, but suspended it completely is now part of my “buy list”! CAE suspended its dividend and its share buyback plan on top of laying-off 2,600 of its 10,500 employees. The company shows about 50% of its revenue coming from civil aviation training. You can imagine that the next few quarters will likely not include any good news (next update to come on May 22nd). The demand for both pilot training and for new simulator time will plummet temporarily.

What could go right?

CAE is a highly innovative company. While the company is facing an important challenge, the company quickly shifted some of its resources to offer healthcare training support regarding the COVID-19 pandemic and it expects to produce about 10,000 ventilators over the next 3 months. Sooner or later, the airlines will reopen and the demand for recurring pilot training will resume. CAE can also count on its defense segment (about 40% of revenue) to generate a constant flow of income in the meantime.

Conviction for the Long Run

There are two strategies you can use to determine your next move. One is based on the current stock price and how it lost value. The other is based on the fundamental reason why you might add (or not add) this company to your portfolio. While the first strategy is widely used among investors, I prefer the latter. A strategy based on an investment thesis will always provide you with great confidence in your picks and will reduce some of the emotions attached to trading. Therefore, it’s always the time to invest according to DSR’s principle.

Since those stocks haven’t recovered their losses, this is a great opportunity to combine both the price and investment strategies together. Keep in mind these are long-term plays. Don’t expect short term gains.

Leave a Reply