Risk is a crazy thing. Take on too much and you either crash and burn or make out like a bandit. Take on too little and you either just float along or make out like a bandit. The “trick” is figuring out the happy medium that you will be comfortable with. I have spent some time determining what my risk profile is and have asked myself several questions…

- Do I prefer stability over high returns?

- How can I make money without risking too much?

- Do I feel bad when all my friends are making double digit

- returns and I’m not?

- My Portfolio is down by 27% (2008), it hurts… how bad

- does it hurt?

- Should I sell my stocks and change my strategy?

- When is the right time to invest in the market? I don’t want

- to invest right before a crisis!

The funny thing is that I don’t have the same risk profile depending on why I invest. Therefore I have different answers to these questions depending on which account I invest in. For example, my retirement account is fairly aggressive. Therefore, when I invest in my retirement account, I’m 100% invested in stocks. I’m in the stock market for the long run and I don’t fear a market crash.

On the other hand, I’m also putting money aside for my kids’ education. I’ve added 25% of fixed income to this portfolio because I don’t want to risk losing too much in this account. Furthermore, I’m also saving money for my nephew’s education. Since this money is set aside for a gift, I have put 75% in fixed income and the rest in equity. As you can see, I manage three portfolios from 100% in stocks (retirement account) to as little as 25% in stocks for my nephew.

The time horizon for your project (that you previously defined) will also affect your investor profile. If you plan a trip in 9 months, skip the stock market and put your money in a savings account. If you are about to retire, you can still take a good amount of risk as chances are you will be living off your investment for 30 years (I bet you didn’t think of this one, huh?).

For each account, you should ask yourself the same question. Contextual reasons may encourage you to take more or less risk. Here’s a quick definition of different investment profile:

Conservative:

You have a need for a predictable flow of income or have a relatively short investment horizon. Your tolerance for volatility is low and your primary goal is capital preservation.

Moderate:

You seek a regular flow of income and stability, while generating some capital growth over time. Your tolerance for volatility is moderate and your primary goal is capital preservation with some income.

Balanced:

You’re looking for long-term capital growth and a stream of regular income. You’re seeking relatively stable returns, but will accept some volatility. You understand that you can’t achieve capital growth without some element of risk.

Growth:

You can tolerate relatively high volatility. You realize that over time, equity markets usually outperform other investments. However, you’re not comfortable having all your investments in equities. You’re looking for long-term capital growth with some income.

Aggressive:

You can tolerate volatility and significant fluctuations in the value of your investment because you realize that historically, equities perform better than other types of investments. You’re looking for long-term capital growth and are less concerned with shorter term volatility.

Action of the day: Setup your investing profile

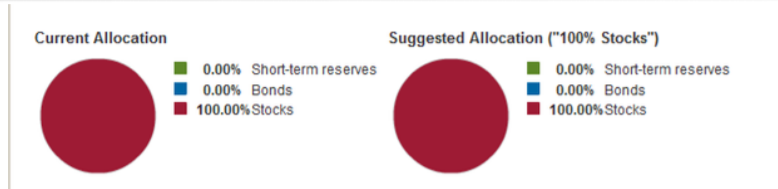

To answer this tricky question, there is nothing better than answering a questionnaire. I’m sure you have answered this sort of thing before. They seem cheesy sometimes but trust me; it will help you put things into perspective. Based on my experience, I feel that most people believe that they are braver than they are! The real investor in you tends to show up when the market crashes. Speaking of which, I found this investor questionnaire over @ Vanguard . I’m in no way linked or paid by this group to refer you to their risk profile questionnaire. I just find it is one of the best around since they help you relate to 11 questions that include practical facts that happened in 2008. With no surprises, I finished mine with a 100% stock profile:

What’s yours?

Nice analysis. Sometimes it is a risky game that we play but it can pay out nicely