Leggett and Platt (NYSE: LEG) has been transforming itself over the last five years into what I believe will be a stronger business going forward. These changes lead to growth figures from the last several years looking unattractive when one looks at the surface data, so digging into the causes is required to understand the situation. I think many investors may like what they find.

-Seven Year Revenue Growth: n/a

-Seven Year EPS Growth: n/a

-Seven Year Dividend Growth: 9.5%

-Current Dividend Yield: 4.96%

-Balance Sheet Strength: Moderately Strong

Leggett and Platt offers one of the larger dividend yields out of the list of companies that have consecutively raised dividends for decades. I believe that in this somewhat richly valued market, Leggett and Platt stock should offer respectable risk-adjusted returns at the current valuation in the low-to-mid $20’s.

Overview

Leggett and Platt (NYSE: LEG) is a designer and manufacturer of a large number of engineered components for home, business, and automobile use. The company was founded in Missouri in 1883. The company operates 130 manufacturing sites in 18 countries with 18,000 employees.

The company is divided into four segments, and each segment is divided into a number of business units.

Residential Furnishings Segment

This segment contributes 50% of total Leggett and Platt sales. For 2011, this segment saw sales increase by over 5%, but the company attributes much of that increase to inflation and currency. Notably, annual growth in adjustable beds was rather large at 44%, which was good for the company. This residential furnishings segment was Leggett and Platt’s original business, and is among their largest and strongest of areas. It consists of mattress springs, bed frames, ornamental beds, seat holdings, the various hardware mechanisms in furniture such as the system that allows for a recliner to recline, and other furnishings.

Commercial Fixturing and Components Segment

This segment produces shelving and display units for a very large number of retailers, and also produces office furniture components. The segment contributed 14% of total 2011 Leggett and Platt sales. Unfortunately, 2011 was not a good year for this segment, as sales fell over 5% mainly due to decreases in volume.

Industrial Materials

The industrial materials segment produces external sales but also provides materials for the other segments of the company. With hundreds of thousands of tons of steel wire produced annually, this segment is the largest producer of drawn steel wire in the country. The segment also produces steel tubes, and erosion-control products, and the total segment contributes 17% of total Leggett and Platt sales. The segment saw a dramatic 23% sales increase from 2010 to 2011, but much of this was due to steel price inflation.

Specialized Products

The specialized products segment produces automotive systems (lumbar supports, control cables, seat suspension, and motor/actuation assemblies), machinery for sewing and wire shaping, and commercial vehicle products (van interior rack systems, trailers, and docking stations). This segment produces 19% of total Leggett and Platt sales, and had the most positive performance in 2011; despite higher material costs, both sales and operating income rose substantially in all three business units, and much of this was due to volume growth. There was, however, impairment from a specific patent write-off.

Sales, Earnings, Cash Flow, and Metrics

Over the last several years, the company has posted rather unimpressive numbers, but much of this was because the company was actively selling off under-performing businesses and giving the money back to shareholders. So they were selling off revenue and income streams, which naturally results in poor revenue and earnings growth. This will be further explained in the investment thesis section, and is part of the aforementioned “transformation”.

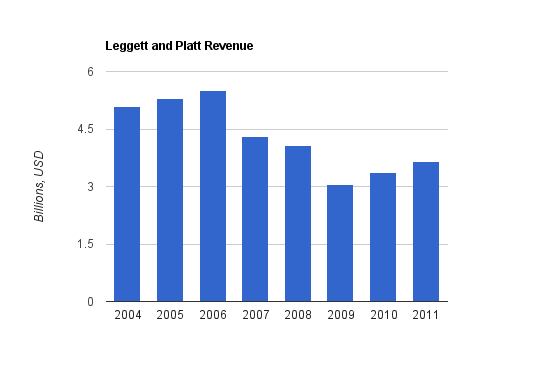

Sales Growth

| Year | Revenue |

|---|---|

| 2011 | $3.64 billion |

| 2010 | $3.36 billion |

| 2009 | $3.06 billion |

| 2008 | $4.08 billion |

| 2007 | $4.31 billion |

| 2006 | $5.51 billion |

| 2005 | $5.30 billion |

| 2004 | $5.09 billion |

As can be seen, Leggett and Platt had sales declines over this period. Even going back further, to 2001, shows that today’s sales levels are lower than they were ten years ago. For the first part of the decade, it was due to flat growth. For the second part of the decade, it was due to selling off businesses, and as can be seen, over the last two years, the numbers have improved.

The company estimates $3.6 to $3.8 billion in revenue for 2012.

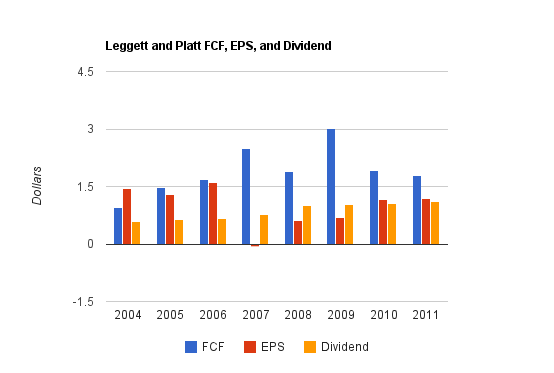

Earnings Growth

| Year | EPS |

|---|---|

| 2011 | $1.20 |

| 2010 | $1.15 |

| 2009 | $0.70 |

| 2008 | $0.62 |

| 2007 | $-0.06 |

| 2006 | $1.61 |

| 2005 | $1.30 |

| 2004 | $1.45 |

Again, no earnings growth, and it’s for the same reason as the lack of revenue growth. The 2011 figure is adjusted to exclude a one-time restructuring charge.

The company estimates EPS of $1.20 to $1.40 for 2012.

Cash Flow Growth

| Year | Operating Cash Flow | Free Cash Flow |

|---|---|---|

| 2011 | $329 million | $254 million |

| 2010 | $363 million | $295 million |

| 2009 | $565 million | $482 million |

| 2008 | $436 million | $318 million |

| 2007 | $614 million | $465 million |

| 2006 | $479 million | $313 million |

| 2005 | $448 million | $284 million |

| 2004 | $343 million | $185 million |

Not much growth here either. The company estimates operating cash flow to again exceed $300 million in 2012. There are two things to notice, however:

A) Strength of Free Cash Flow (FCF) was inversely proportional to earnings. During the period of poor EPS, FCF was through the roof. This was related to the selling-off of businesses.

B) If one compares FCF to net income for a given period, one will see that FCF is much higher. I didn’t present a net income table above (as I presented the EPS table instead), but for example in 2011, the company reported $153 million in net income and $254 million in FCF. The primary reason for FCF being so much higher is due to the large non-cash depreciation.

Metrics

Price to Earnings: 19

Price to Free Cash Flow: 12

Price to Book: 2.4

Return on Equity: 12.5%

Dividends

Leggett and Platt has increased its dividend every year for four consecutive decades. The company currently offers a dividend yield of just shy of 5%, has a dividend payout ratio from earnings of 90%, and has a dividend payout ratio from free cash flow of 60%.

Dividend Growth

| Year | Dividend |

|---|---|

| 2011 | $1.10 |

| 2010 | $1.06 |

| 2009 | $1.02 |

| 2008 | $1.00 |

| 2007 | $0.78 |

| 2006 | $0.67 |

| 2005 | $0.63 |

| 2004 | $0.58 |

Over this period, Leggett and Platt has grown the dividend at a 9.5% annualized rate. Much of this growth was between 2006 and 2008, when the company actively sold off several businesses and dramatically increased what was already a fairly robust dividend. I expect future dividend growth to be in the low to mid single digits, which when combined with the fairly significant dividend yield, is quite reasonable.

Dividend Safety

The dividend payout ratio from earnings should rightly be a red flag for any astute dividend growth investor. But as one can see, the payout ratio from FCF is only around 60%.

From the earnings payout ratio, it may appear that Leggett and Platt is having trouble keeping up with their dividend, but this is not the case. In fact, in 2011, the company paid out $157 million in dividends, and $205 million in net share repurchases (meaning shares repurchased minus shares issued). And they’ve been doing large share repurchases in all recent years. That’s their policy- provide a large dividend, and then use the rest of their substantial cash for either share repurchases or acquisitions.

The interesting thing to point out is that Leggett and Platt has been growing the dividend per share, without growing the total dividend payout, for years now. In 2011, the company paid $157 million in dividends. In 2010, they paid $155 million. In 2009, it was $157 million. In 2008, it was $165 million. (Before that, the total dividend payout was increasing). But during this period, they were growing dividends per share because they were spending even more money on share repurchases compared to dividends, so they were reducing the total number of shares. The company has reduced the number of outstanding shares substantially since 2007, and this has allowed the company to pay out basically the same total dividend, while simultaneously increasing the dividend on a per-share basis. So their dividend growth and payout situation is under control.

So this is one of the few companies that I think puts share repurchases to good use, since they pay a large dividend first, and then use remaining cash more flexibly for either acquisitions or share repurchases. A special dividend could potentially be in place of the repurchases, but overall, I think Leggett and Platt is doing a great job here so there’s not much to complain about.

Their dividend payout ratio is indeed above their target, since the market contracted on them. But as can be shown by the numbers, they’re easily able to support the dividend as well as share repurchases. Their target yield is 3-4% rather than 5%, so I’d expect that over the next few years, we’ll see only small dividend increases until share repurchases and acquisitions reduce the dividend payout as a percentage of earnings and FCF.

Balance Sheet

The total debt/equity ratio is under 65%, the interest coverage ratio is over 7, and the total debt/income ratio is around 5. Goodwill makes up a fairly substantial amount of shareholder equity.

Overall, I consider these numbers very solid for this industry. The company is making good use of leverage but with a lot of room for safety. Manufacturing is an asset-heavy business, so debt/income is going to naturally be a bit higher than some other industries.

Investment Thesis

When one looks at the numbers over the last ten years, and sees lack of revenue growth, lack of EPS growth, and strong dividend growth but a high dividend payout ratio from earnings, many investors would understandably move on. Afterall, one does not want a declining business, and experienced dividend growth investors know better than to chase yield.

However, Leggett and Platt has transformed itself over the last five years, and now I believe the company will be a better-positioned business for shareholders. The revenue and income declines were due to divestitures, and now that they’ve been done for over a year, I’m interested in the company’s future.

The Transformation

Up until 2006, the company was doing ok, but could be said to be stagnating a bit. Their business model focused mostly on growth. The company wasn’t under serious pressure since they were still profitable, but their model of capital allocation wasn’t optimal anymore. The company had performed very well for so long, with decades of consecutive dividend growth (and only 8 CEOs between 1883 and 2006), but was temporarily under-performing.

In 2006, a new CEO, David Haffner, was appointed. In 2007, he announced a new strategy, which consisted of the following:

1. Divest low-performing business units, or units that do not align with LEG’s core strengths.

2. Return more cash to shareholders.

3. Improve margins and returns.

4. Grow the company at 4-5% annually.

And this is what he has done. He substantially boosted the dividend yield, started reducing the number of shares, and has divested some of the under-performing business units and seeks to acquire higher-margin businesses.

Before Haffner, Leggett and Platt was holding a collection of business units, allocating them capital, and expecting them to grow. Haffner, however, sold off numerous business units that were either under-performing, low-margin, or where Leggett and Platt simply didn’t have any competitive advantage (examples include coated fabrics, fibers, wood products, plastics, foam products, and certain other things). The remaining 20 business units are now managed much more intentionally: each business unit in the portfolio of business units is labeled as “Grow”, “Core”, “Fix”, or “Divest”. (Previously, they were all just “Grow”.) Growth business units are allocated capital and expected to grow. Core business units are healthy and profitable businesses where Leggett and Platt has economic advantages, but with less growth potential, where the company will withdraw large amounts of free cash flow and not need to invest much capital to maintain or modestly grow the unit. Most of the businesses are Core. Fix and Divest business units are self-explanatory; they’re business units that the company is looking to repair, or business units that they are actively marketing for sale to another company.

Overall, this is a much more intentional and streamlined Leggett and Platt. This process helps ensure optimal use of capital.

One could draw numerous comparisons between Leggett and Platt, and Ford Motor Company. Although Leggett and Platt was not nearly under the same distress as Ford, both of the companies appointed new CEOs around the same time that began divesting businesses and streamlining their remaining businesses. I’m bullish on both of these companies and think that both of them have excellent CEOs.

Leggett and Platt management states that their goal is to provide returns that fall within the top third of the S&P 500 companies.

They plan to do this through:

4-5% annual sales growth

3-4% dividend yield

2% improved margins

3-4% stock buybacks

Which is a total annualized target of 12-15%, but doesn’t take into account changes in stock valuation (since management has no control over that).

Now, whether they’ll reach those precise numbers or not is yet to be seen, but I love that split of areas of growth. The current CEO is an executive that dividend growth investors should love. And these targets provide a decent margin of safety, since even a rate of return that falls under 12% is very acceptable.

Western Pneumatic Tube Acquisition

Leggett and Platt has a very specific list of things they are looking for in acquisitions. In summary, they want businesses that fit into their existing strengths, that have competitive advantages from patents, or processes, or differentiation, or special skills, and that meet certain quantitative criteria.

That being said, they recently made their first major acquisition since 2007. They acquired Western Pneumatic Tube for $188 million in January of this year. This company brings in about $60 million in revenue, and makes specialty titanium and nickel tubes for the aerospace industry. Leggett and Platt listed numerous reasons for the acquisition, including:

-The company has higher margins than is the average for Leggett and Platt business units, so it will have a positive impact on margins.

-The company produces specialized (non-commodity) products, and there are high barriers of entry due to the certification process that’s needed for such mission-critical systems in the aerospace industry.

-It fits directly into one of Leggett and Platt’s core competency areas of metal tubing, and the quality and timeliness requirements are facilitated by Leggett and Platt’s large scale and logistics competencies.

-Systems in this industry have very long produce lifecycles; suppliers generally are not switched out very often.

The key risks are a) exposure to cyclical aircraft industry and b) customer concentration.

The company has other growth areas for the specialized tubes as well, ranging from solar energy to chemical processing.

On the other side of the coin, Leggett and Platt divested their small U.K. display business unit. This falls into the strategy of focusing on core areas and managing their portfolio of businesses proactively and intentionally.

Economic Moat

I view Leggett and Platt, as well as numerous other businesses in its peer group including Dover Corporation (DOV), Emerson Electric (EMR), and Illinois Tool Works (ITW), as having a decent, if not huge, economic moat. I’ll be talking about this industry a bit in my upcoming dividend newsletter.

First, after the strategic divestitures, Leggett and Platt is the largest producer in most of its areas of operation, despite only having a market capitalization of a bit over $3 billion. They sold off business units that were distractions for them to focus on their core competencies. Their competitors are generally small and not publicly traded. Plus, the company is rather vertically integrated, meaning that as previously mentioned, their own industrial materials segment provides for most of their steel material needs. So their whole process is difficult to replicate by a competitor.

Second, the company has a substantial patent shield, with 1,100+ issued patents and another 400+ patents in process.

So between scale and patents, they have considerable economic advantages. They look for similar attributes in acquisition targets.

Risks

Leggett and Platt does have some risks. There are the common risks of inflation of commodity prices, decrease in customer demand, currency changes, and so forth. It’s also worth discussing some more specific risks.

For one, a principle business of theirs is to make mattress springs. These systems have a very strong share of the market for beds, but increasingly on the higher-end, there are more beds that are not based on mattress springs. In the most recent earnings call, Karl Glassman, Chief Operations Officer of Leggett and Platt, discussed the industry a bit. He estimated that 10% of bed units in the market are alternative/speciality units, and that due to the premium price, this makes up 25-30% of dollars spent. This risk is manageable for a number of reasons. Firstly, these are generally expensive beds. Nine out of ten beds are still the kind that Leggett and Platt focuses on. Secondly, even if this market expands, a significant percentage of alternative/specialty units are “hybrid” beds. These hybrid beds are not all foam, but instead utilize spring systems (often supplied by Leggett and Platt), along with some of the higher-end materials. So although there’s a concern that a greater percentage of beds could be in areas where Leggett and Platt does not have a competitive advantage, the combination of their strong market share in springs, their strong market share in hybrid beds, and their diversification into numerous other businesses, supplies confidence.

Two, the recession along with an increasing income/wealth gap in the U.S. could hurt or benefit the company. It could prevent the purchases of those aforementioned higher-end beds (which is nice for the spring industry), but it could also delay the purchase of all beds and furniture, and convince consumers to hold onto older furniture for longer. Leggett and Platt management has reported an interesting observation over changes in long-term trends in their latest earnings call: it used to be that the biggest months for bed purchases were in the autumn, but now, the biggest months are in the late winter, which is highly correlated with tax return season.

Overall, I view Leggett and Platt’s risk/reward profile to be fairly strong.

Conclusion and Valuation

In conclusion, the surface numbers for the company can be misleading, and Leggett and Platt is worth a close look as a dividend stock portfolio candidate.

-The company has divested numerous businesses and has given that cash back to shareholders. The company is a lot more streamlined and intentional now.

-The dividend is safer than the dividend/earnings payout ratio would imply, due to the strong free cash flows.

-Now that divestitures have been completed, the company looks for growth, and has performed a new acquisition.

There are some risks, and investors may have differing opinions regarding the attractiveness of Leggett and Platt stock, but the important thing is that any analysis should take into account quantitative and qualitative changes in the company, and should base estimates on forward growth rather than past growth.

When it comes to valuation, there are numerous estimates one could make that involve free cash flow growth and the percentage of free cash spent on acquisitions, as well as use a few different discount rates. Using a 4% free cash flow growth rate and an 11% discount rate, I calculate that the stock is slightly undervalued. But subtracting acquisition costs from FCF, or using a 5% growth rate, or tweaking the discount rate, can provide a range of estimated intrinsic values. Overall, taking everything in this analysis into account, I view the stock as reasonably valued for purchase. A few weeks ago, the stock had an 8% daily drop due to the mixed earnings announcement, so I picked up shares with a dividend yield of above 5%. The stock has since rebounded a bit, but I still think it’s appealing.

Full Disclosure: At the time of this writing, I am long LEG and EMR.

You can see my dividend portfolio here.

[…] for shareholders. It’s notable that several businesses such as Emerson Electric (EMR), Leggett and Platt (LEG), Dover Corporation (DOV), and Illinois Tool Works (ITW) are in rather cyclical industries and […]