Kinder Morgan Inc. (NYSE: KMI) holds the general partners of Kinder Morgan Energy Partners LP (KMP) and El Paso Pipeline Partners LP (EPB).

![]()

-Current Distribution Yield: 3.86%

-Balance Sheet Strength: Highly Leveraged, Stable

As a general partner, KMI has a lower dividend yield but a higher expected dividend growth rate than KMP, and is positioned to have more risk (with greater financial leverage and structural leverage) and also the potential for a higher rate of return.

Overview

Kinder Morgan Inc. (NYSE: KMI) holds the general partner units and considerable portions of the limited partner units of both Kinder Morgan Energy Partners LP (KMP) and El Paso Pipeline Partners LP (EPB). Most of the income comes from LP distributions and Incentive Distribution Rights (IDRs), although the company does also hold assets directly that it plans to drop down to the partnerships.

Kinder Morgan Energy Partners LP (KMP)

The largest holding of KMI is its interest in KMP/KMR. It holds the general partner and over 10% of the limited partner units.

KMP owns interest in or operates tens of thousands of miles of pipelines and 180 terminals, making it one of the largest of energy businesses, and the largest midstream business, in the United States.

The partnership has a variety of business segments, including natural gas pipelines, CO2, terminals, and product pipelines.

For the full article, see the recent KMP Analysis.

El Paso Pipeline Partners LP (EPB)

More recently, KMI holds the general partner of EPB and over 40% of the limited partner units. EPB is a bit over 1/4th the size of KMP, so it’s a smaller contributor for KMI’s income.

EPB focuses specifically on natural gas, with pipelines in the southeastern United States and in the Rocky Mountain region, along with gas storage areas and LNG terminals.

Because of EPB, an investor in KMI has a larger amount of exposure to natural gas than an investor in KMP. Less than 40% of the business mix of KMP is based on natural gas pipelines, while over 50% of the business mix of KMI is based on natural gas pipelines, due to the influence of EPB.

Business Mix

KMI has a significant focus on natural gas, but the other half of the business mix is rather diversified.

Natural Gas Pipelines- buying, selling, transporting, storing, gathering, and processing natural gas

Segment earnings: 54%

CO2- transporting and selling CO2

Segment earnings: 20%

Terminals- transloading, storing, and delivering bulk (including steel and coal), petroleum, and chemical products

Segment earnings: 12%

Product Pipelines- transporting, storing, and processing refined petroleum products

Segment earnings: 11%

Kinder Morgan Canada- petroleum pipelines

Segment earnings: 3%

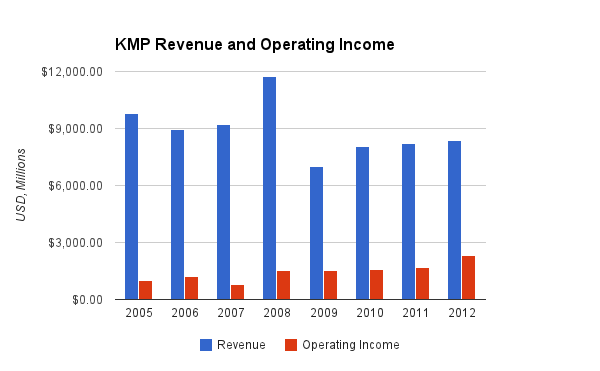

Revenue and Assets

KMI generates its own income from the stakes it holds in the Kinder Morgan and El Paso Pipeline assets.

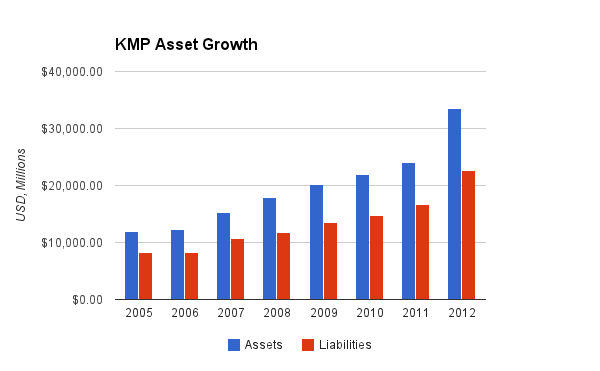

(Chart Source: DividendMonk.com)

(Chart Source: DividendMonk.com)

In addition, EPB currently produces over $1.4 billion in annual revenue. The total revenue for KMI’s underlying partnerships as a whole is over $11 billion.

Dividend Growth

Since KMI has been publicly traded under its current form only since 2011, dividend history is minimal. The final quarterly dividend of 2012 was 20% higher than the final quarterly dividend of 2011. KMI’s budgeted dividend for 2013 is $1.57/share, which is around 17% higher than the 2012 figure.

If KMP and EPB continue to perform well, KMI’s overall dividend growth should outpace both of them.

Balance Sheet

Kinder Morgan Inc. is a highly leveraged entity. On some articles/comments, I’ve seen some questions about general partners and some of their debt metrics (primarily questions about why the debt metrics are so bad), so it’s worth clarifying.

A partnership is itself a rather leveraged entity. KMP and EPB are asset-heavy businesses with stable cash flows and generally very long term contracts, and as such, they use quite a bit of debt in order to attain a solid rate of return. The above KMP asset chart shows the consistency witch which they apply leverage over time.

So KMI holds the general partner interest, incentive distribution rights, and other assets such as limited partner units of both KMP and EPB, and therefore has exposure to that leverage. On top of that, KMI has its own debt. The long-term debt of KMP and EPD sums to about $20 billion while KMI has another $10+ billion debt.

The closest comparison is to say that it’s like buying shares of stock on margin. If you own a share of stock worth $100, and you use $80 of your own money and $20 in debt to buy it, then you’ve got $80 in equity out of the $100 in assets. But really, that $100 share of stock likely has a book value that is lower than $100. If the price/book ratio is 3 for example, then the book value of that share is only around $33, so with that calculation, your actual ratio of debt to assets is much higher.

This is how general partners tend to work. They hold a stake in “assets”, but those assets are really a combination of assets and liabilities. And then on top of it, they use debt to buy those assets. So KMI and other publicly traded general partners tend to have seemingly terrible ratios for debt/equity when the layers of debt are put together. This is not a result of a poorly run business, and not a sign of a company that’s out of control, but rather a natural aspect of how publicly traded general partners operate.

It is a complex and leveraged structure, but it remains stable as long as KMP and EPB continue to perform well.

Investment Thesis

General partners such as KMI can offer outsized returns. Richard Kinder holds his assets in KMI, and it has potentially the most privileged position out of all of the different ways to buy into this entity as long as the entity continues to perform well.

Here’s the breakdown of where KMI received its income over the last quarter:

Distributions Received from KMP, KMR, and EPB

| KMP General Partner Distributions | 72% |

| KMP/KMR Limited Partner Distributions | 10% |

| EPB General Partner Distributions | 8% |

| EPB Limited Partner Distributions | 10% |

As can be seen, the general partner distributions of KMP play a dominant role in KMI’s total income and dividend-paying potential. This is primarily from the Incentive Distribution Rights (IDRs). KMI’s most valuable holdings are the 100% IDRs in KMP and EPB.

The reason holding a GP can be so lucrative has almost entirely to do with the IDRs. Master Limited Partnerships are designed to be fast-growing, distribution-paying machines. The structure is inherently optimized for it. IDRs dictate what percentage of the total partnership cash flow the general partner receives, and it’s based on two main factors: distribution growth and overall growth.

The IDRs are set up in tiers. Once certain distribution targets are reached for KMP and EPB, KMI is entitled to a larger portion of the total cash flow. In addition, they benefit when a larger number of units are issued to grow the overall partnership, because they get a percentage of a larger pie of cash.

As KMP and EPB increase their number of units and increase their distributions, the unitholders of those entities benefit from increased distributions. But KMI unithholders benefit both from the increases in distributions (since according to the IDRs they get a larger share of the total cash flow) and from increases in the overall number of units and partnership growth (because the total cash flow from which they derive their percentage increases). This is why a well-run partnership can result in better returns for the holder of the general partner and incentive distribution rights.

KMP is a very mature partnership and so it has already reached its high tier distribution targets. Over 40% of KMP’s available cash gets paid to KMI simply due to the IDRs (which accounts for over 70% of KMI’s incoming distributions). Currently El Paso Pipeline Partners IDR distributions only account for around 8% of KMI’s total incoming distributions, but this segment can grow much larger as EPB continues to issue more units and expand its overall asset base.

Risks

KMI’s structure is its source of good potential returns and large potential risk. As an entity with multiple layers, a failure on the foundation of the overall entity can bring down the top. There is risk from large accidents, and changes in interest rates play a big role for profitability. A 100-bp increase in interest rates increases KMP’s interest expense by $55 million, EPB’s interest expense by $4 million, and KMI’s interest expense by $35 million, according to a December 2012 presentation by David Kinder.

With KMI debt on top of the already leveraged partnerships, KMI is highly leveraged. The biggest component of the income comes from KMP incentive distribution rights payments. A large failure in KMP to the point of having to cut the distribution would have an even larger impact on KMI, since their IDR payments would fall even more than the cut to KMP unitholders. So KMI is highly financially leveraged and highly structurally leveraged.

That being said, the assets that produce KMI’s income are highly diversified. It’s one of the largest energy companies in North America, and it has been exceptionally well run for 15 years. The natural gas pipelines, product pipelines, CO2 pipelines, and terminals are spread across much of the United States and into Canada. Long-term contracts and/or regulation are in place for much of their cash flows.

So overall, KMI is highly leveraged on a diversified and stable base of assets and cash flows.

Conclusion and Valuation

Using the Dividend Discount Model, KMI only needs 8% long-term dividend growth in order to justify the current price using a fairly aggressive 12% discount rate (target rate of return).

Due to the leveraged nature of the business, above average returns should be sought. If the two partnerships are managed well, KMI unitholders should expect robust returns over the next several years. The cost of this opportunity is that any setbacks for these partnerships, however unlikely, could have larger negative effects for KMI.

Overall, I consider KMI attractively valued with a sufficient margin of safety at the current price of under $38.

Full Disclosure: As of this writing, I am long KMI.

You can see my dividend portfolio here.

Strategic Dividend Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

I appreciate your annotation of graphs, charts, and terms…. very much. Thanks and Regards.

Thanks for the analysis on KMI. I’m long KMI and am looking forward to the future dividend growth. Richard Kinder is someone I’ll side with.

Thanks for all your great analyses. I also picked up some KMI within the last few months. KMP also looked attractive with its higher yield, but once I realized that KMP’s distributions would be subject to a 35% withholding tax (I’m in Canada), while KMI’s (potentially faster-growing) dividends would have no tax withheld (in an RRSP account), the choice became a lot easier.

Yes, an addition to the article would be to point out that another key difference between KMP and KMI is that KMP is an MLP while KMI is a c-corp. So there are different tax treatments domestically and internationally.

I am a fairly novice investor looking to add a decent yielding energy company to my portfolio but I am scared off by all I read about MLPs having difficult to deal with tax implications. My portfolio is in a taxable account not an IRA. Can you explain in layman’s terms what the different tax treatments are domestically for KMP vs KMI, and which one would be a better choice for me?

Owning an MLP means you will receive a K-1 form before you prepare your taxes. The reason is, an MLP doesn’t pay tax like a corporation; it’s merely a pass through entity. So each year,a team of accountants do the tax work for the MLP and send you a form that lists your personal share of the profits based on the number of units you own, and you need to use this form when you fill out your personal income taxes. It’s different than just paying capital gain taxes and dividend taxes.

The downsides of this are that the information usually comes a bit late so you may not be able to get your taxes done early, it’s something extra to do, and in large cases, you can technically owe taxes to places where the partnership has done business. To several states. The upside is that, quantitatively, it’s usually a tax-advantaged situation. Most of the taxes end up getting deferred until the units are sold, so compared to regular stock after all layers of taxes are considered, you’ll generally pay less taxes.

KMP is an MLP, so if you own it you’ll receive a K-1 form and will have to file those taxes.

KMI, on the other hand, is a C-Corp. It’s a regular corporation like Johnson and Johnson or Procter and Gamble. They hold stake in the partnerships but they themselves are structured as a corporation. So as a shareholder in KMI you would have no differences in taxes for KMI compared to any other stock like JNJ or PG. You pay capital gains and dividend taxes like usual.

There is no definite better choice for you. First of all, they differ in far more ways than just the taxes, so those aspects need to be considered. Second, it depends on your priorities. If you’d like to keep your taxes as simple as possible, KMI is better in that area.

Thanks. I will be looking to add KMI to my portfolio soon.

We sold KMI and received a K-1 form from them. We are an investment club and need advice as to what to do with the partnership distribution.

I own KMI and KMR. I like the above average yield for KMI as well as the opportunity for double digit dividend increases. I think that with the completed El Paso acquisition we are going to see high dividend growth. My concern with MLPs is that at some point, we would see oversaturation, and companies like KMI would start overpaying for assets..

I agree. El Paso’s IDRs are a huge area of potential growth for both its unitholders and KMI’s unitholders.

I do think over-saturation is potential problem. MLPs are designed to grow like wildfire, so it remains unknown how long the industry as a whole can grow for. Kinder has an excellent track record for management, so I’d imagine that even if some partnerships do overpay for assets, KMI would be fairly resistant to those trends.

Matt,

Great analysis here. I appreciate the amount of time you spent on the balance sheet, as the leveraged nature of this business required extra attention and explanations. Great job!

I agree with you on the overall investment thesis (attractive assets, long-term contracts) and the valuation, as well as the inherent risks (interest rate risk, accidents, black swans). I also agree with you that the risk/reward profile with this one is bit more aggressive than say a Coca-Cola, but the chance for outsized returns is, in my opinion, good enough to invest in KMI.

Best wishes!

Very nice analysis of KMI. I thought that your explanation of the balance sheet and use of leverage was well done.

I remain interested in KMI and am considering a position myself. But I’ve got a number of energy stocks right now, so I might put off buying KMI in favor of better diversification. Depends a bit on my mood and a bit on which stock is trading at a nice price.

Has anyone developed a spreadsheet to calculate capital gains for 1040 taxes and calculate the new basis regarding the 2012 el paso (ep) and kinder morgan (kmi) merger?