Colgate-Palmolive Company (NYSE: CL) is a $56 billion market-cap consumer products company with strong market share in tooth paste and soap.

-Seven Year Revenue Growth Rate: 6.0% ![]()

-Seven Year EPS Growth Rate: 11.3%

-Seven Year Dividend Growth Rate: 11.9%

-Current Dividend Yield: 2.25%

-Balance Sheet Strength: Strong

Colgate’s strong product appeal and unusually wide global reach (even among American blue-chips) give investors a lot to like, but the fairly high stock valuation of the company keeps the dividend yield on the lower side and reduces or eliminates any margin of safety.

Overview

Colgate was founded in 1806 in New York as a soap and candle company. Colgate-Palmolive is now a multinational corporation selling oral hygiene products, soaps, and pet nutrition products. The company currently has a market capitalization of over $56 billion.

Business Segments and Divisions

Colgate-Palmolive consists of four business segments: Oral Care, Personal Care, Home Care, and Pet Nutrition.

Oral Care

Oral Care represents 44% of total company sales, which includes their flagship Colgate brand as well as Tom’s of Maine. According to a recent investor presentation, the company has #1 market share in 146 countries, which makes it the world’s leading oral care brand.

Personal Care

The company’s second largest segment is their personal care segment, which accounts for 22% of sales. This segment includes the leading Palmolive soap brand, as well as other brands such as Irish Spring and Speed Stick deodorants. The company claims the #1 market share spot worldwide for liquid hand soap and the #2 spot for bar soaps.

Home Care

The home care segment accounts for 21% of sales, and includes Palmolive dish soap and a set of small and medium brands. The company claims the #1 global spot for dish soap and the #2 spot for fabric conditioners and household cleaners.

Pet Nutrition

Approximately 13% of sales come from the Pet Nutrition segment. Their two big brands here are Science Diet and Prescription Diet, and while they are not the top brands overall, they do claim #1 market share in vet clinics worldwide. The products are sold primarily through veterinarians and specialty pet food stores, and the products are available in 90+ countries.

The company can also be understood as consisting of five geographic business divisions (or, more accurately, four geographic divisions plus Pet Nutrition)

North America

The North American division represents 18% of total company sales.

Latin America

The Latin America division represents 29% of sales.

Europe/South Pacific

The Europe/South Pacific division represents 20% of sales.

Greater Asia/Africa

The Asia/Africa division represents 20% of sales.

Hills Pet Nutrition

The Hills Pet Nutrition segment represents 13% of sales, as previously described. This segment is always grouped separately from their geographic segments.

Ratios

Price to Earnings: 25

Price to Free Cash Flow: 21

Price to Book: 32

Return on Equity: 115%

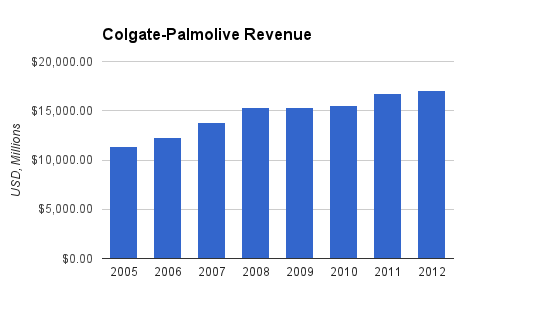

Revenue

(Chart Source: DividendMonk.com)

Revenue grew at a very solid 6% per year on average over this period. This revenue growth is what appears to be driving the stock’s high valuation.

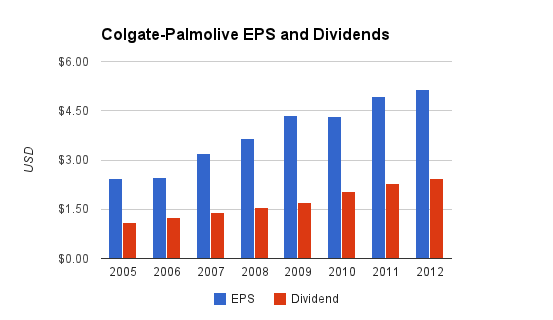

Earnings and Dividends

(Chart Source: DividendMonk.com)

The EPS growth rate over this period averaged 11.3% per year, which for a blue-chip stock is quite substantial.

The dividend has increased each year consecutively for decades and currently has a payout ratio of approximately 50%. The rather high valuation of the stock has pushed the yield to a fairly low 2.25%. The dividend growth rate over the last seven years has averaged 11.9% per year.

Approximate historical dividend yield at beginning of each year:

| Year | Yield |

|---|---|

| Current | 2.25% |

| 2012 | 2.5% |

| 2011 | 2.7% |

| 2010 | 2.2% |

| 2009 | 2.4% |

| 2008 | 1.8% |

| 2007 | 2.0% |

| 2006 | 2.1% |

| 2005 | 1.9% |

Colgate Palmolve’s yield is in line with where it has been over the last several years. Despite being rather highly valued, it is not out of line of where it has historically been valued. The stock has offered solid returns over this period because the stock price has at most times been supported by fundamental outperformance.

How Does Colgate Palmolive Company Spend Its Cash?

Over the last three years, the company reported a sum of approximately $7.6 billion in free cash flow. Over the same period, $3.6 billion was spent on dividends, $5.8 billion was spent on share buybacks, and about $1 billion was spent on net acquisitions. The buybacks have resulted in a continuously shrinking outstanding share count, but the consistently premium stock valuation has minimized the overall value of these buybacks. Over the last seven years, the company has reduced its share count by about 13%.

Balance Sheet

The company has a total debt/equity ratio of approximately 300%, which is rather high. Furthermore, the amount of goodwill on the balance sheet exceeds the shareholder equity. At first glance, this appears to be a heavily leveraged balance sheet.

The total debt/income ratio, however, is only about 220%, which is rather low. The interest coverage ratio is nearly 50x, which is extremely high, and indicative of an unusually strong balance sheet. The company has very high credit ratings.

The reason for the high debt/equity ratio (and along with it the unusually high price/book value and unusually high ROE), is not that the company has a lot of debt, but rather that the company has a comparatively small asset base compared to the revenue and other figures. Colgate Palmolive has only approximately half as much value in non-current assets as their annual revenue, whereas Procter and Gamble, for example, has significantly more reported value in their non-current assets than their annual revenue.

This small reported asset base keeps the company’s shareholder equity very low, which skews the book value, ROE, and debt/equity metrics upwards. Overall, Colgate-Palmolive has a very strong balance sheet.

Investment Thesis

Colgate-Palmolive is in a very strong position compared to its peers. The company’s early move into developing markets has paid dividends, literally and figuratively, because strong performance in those areas is what is driving the company’s substantial revenue growth.

Even among American blue-chip companies, which tend to have significant international exposure, Colgate-Palmolive is an atypically geographically expanded company. Three-quarters of the revenue is generated outside of North America.

In particular, the Latin America and Asia/Africa regions are enjoying rapid expansion. Their sales growth in Latin America has averaged over 12% per year over the last seven years, and their Asia/Africa region has grown at nearly 10% per year over the same period.

The company complements its traditional mass-marketing branding with brands that focus on natural or sustainable aspects to appeal to certain customers. The acquisition of Tom’s of Maine, for example, gives the company a portfolio of products that attempt to be better for the environment and use more natural ingredients.

Oral care products typically carry high profit margins and customer loyalty. The relatively high price per ounce of branded toothpaste, combined with the rather infrequent need to purchase it (and therefore less of a need to compare prices or buy primarily based on price) as well as the unique taste or characteristics of toothpaste that results in frequent repurchase of the same type, gives the Colgate brand quite a bit of strength compared to other product categories of comparable consumer companies.

Risks

Like any company, CL has risks. Their business is fairly recession-resistant, offering high quality basic products, but they face continual risk from foreign exchange rates, commodity costs, and cheaper product alternatives, as well as strong competition from other top brands including from Procter and Gamble, a larger company. The company spends nearly $2 billion per year on advertising to allow them to maintain or grow their market share.

No single customer represents 10% or more of total sales, and no single supplier or packaging material represents a large percentage of total material requirements of the company.

The place where risks for this kind of company would typically manifest themselves are in the profit margins. Increasing advertising costs and increasing commodity costs can squeeze profit margins and reduce income growth.

Conclusion and Valuation

Overall, I view Colgate-Palmolive as a particularly strong dividend-grower, with high and increasing profit margins, solid revenue growth, wide international reach, and reasonable product diversification.

The question, then, is whether the fairly high price is justified. In order to achieve a 9% rate of return over the long-term based on the Dividend Discount Model, the company would have to grow the dividend by an average of nearly 7% per year for the foreseeable future. If a 10% rate of return is desired, the dividend growth rate would have to be closer to 8%. Colgate-Palmolive has maintained this level of EPS and dividend growth historically, but as it grows larger and saturates its core areas, it may be unable to continue that level of growth.

A reasonable scenario for the company is 2-3% core growth, 2-3% inflation (resulting in 4-6% revenue growth), stable profit margins (resulting in 4-6% net income growth to match revenue), 2-4% worth of the market cap being repurchased annually (resulting in 6-10% EPS growth), and a stable dividend payout ratio (resulting in 6-10% dividend growth) puts it in line with the required sustainable dividend growth rates to justify the current price.

There is not a substantial margin of safety built into the stock price, nor is the current yield particularly desirable. I believe total long-term returns should be reasonable for the foreseeable future, but there are likely superior combinations of income and growth available.

Full Disclosure: As of this writing, I have no position in CL.

You can see my dividend portfolio here.

Strategic Dividend Newsletter:

Sign up for the free dividend and income investing newsletter to get market updates, attractively priced stock ideas, resources, investing tips, and exclusive investing strategies:

thanks for a good analysis, are you also finding good values harder and harder to find?

Yes, over the last several months valuations have been rather substantial. I’ve pointed out what I consider to be a few value stocks in some recent articles, but they’re not very abundant as far as I can tell.

I like Colgate as a business, and own the stock, but would not be adding at current valuations. I would consider adding to my position on dips below $108/share. My last addition was below $93/share in 2012.

That being said, I have no problem holding on to Colgate even if it went to $150 – $160 this year. With forward earnings estimates of $5.72 for 2013, a valuation around $115 might be reasonable.

I like CL and find myself checking in on it every so often. But it’s almost always too overvalued for me to buy. Maybe if there’s a big price dip, I’ll initiate a position.

Thanks for the analysis!

I also like CL a lot but right now, the relatively high P/E ratio makes me doubt it’s a good timing to buy this stock. Do you think CL has been overpriced due to the fact that it’s a very stable business paying a steady dividend better than bonds?

I considered it highly valued a few years ago, and stayed away from ever picking up shares, and it still performed very well. The particularly strong performance justified what was a fairly high valuation.

I don’t view it as currently overpriced, just highly priced with little margin of safety. I’d buy CL over bonds, because it seems to be positioned to offer better long-term returns. But compared to other stocks, the fairly low yield and high valuation keeps me away for now.

CL is one of those companies that is at the top of my “want list.” However, I agree with you that currently it is a little over valued and I personally think there are a few better opportunities at the present moment.

I think we just have to be patient and one day will be able to pick up some shares either undervalued or at least more fair valued. In the meantime patience is key!

Matt,

Appreciate the analysis as always. Not a lot to dislike about Colgate-Palmolive. A solid company with bulletproof products. It’s unfortunate that the market seems to rarely offer a discount on this stock. It appears that CL is perennially expensive. I looked at it when it was about $80 and just couldn’t make the leap. Now I wish I would have jumped in feet first.

Definitely tough to find value out there right now. I find most of it in energy and technology. A smattering of banks. That’s about it. It’s difficult to allocate capital anywhere other than my cash account right now.

Best wishes!