How do you generate income? Yield or Growth? Why Not Both?

When generating income from a portfolio, some may encourage you to utilize high-yielding stocks. You have a million dollars, invest in 7% dividend payers, and earn $70K per year. That’s what I call “napkin calculations.” It’s easy to understand, straightforward and quite appealing.

It’s also incredibly misleading. Dividend cuts happen constantly, and then you lose both your income and capital. You want to avoid that as a retiree.

Others may tell you how they invested most of their money in Tesla and became rich. This is also easy to understand, straightforward, and quite appealing.

But it’s also tough to repeat. It’s fun to play Monday morning quarterback, but when it’s time to pick the next stock that will generate 10X growth, many crystal balls get broken, and investors are disappointed.

Dividends and capital gains are NOT guaranteed. One is not better than the other.

The solution is to find a combination of dividend-paying companies and high-growth companies. This is what I call dividend growth investing.

At Dividend Stocks Rock (DSR), we tend to favor companies with a 4-5% dividend yield and decent dividend growth that at least beats inflation for income-seeking investors. In some rare instances, you will find retirement stocks with more than a 6% dividend growth rate that will keep up with inflation and increase your paycheck yearly.

Find quality income investments

No matter what you do with your portfolio, do not just go for the yield. Don’t get me wrong, it’s okay to have higher-yielding stocks in your portfolio. With the proper research, you can find companies that won’t let you down and keep their generous dividends growing. But that’s not all of them. Go for quality and dividend safety first.

Your asset and sector allocation will explain most of your portfolio return. Since I’m a passionate dividend growth investor, I’ll leave the asset allocation and bond discussion for another day and concentrate this section on sector allocation.

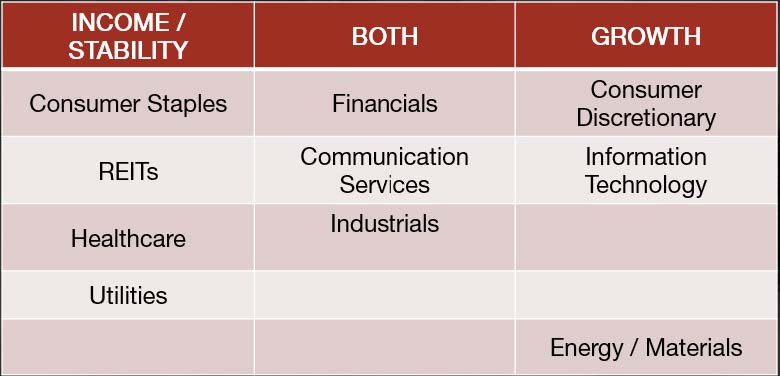

In short, there are 11 sectors that could be qualified under three categories:

Income/stability: Where you will find many mature businesses that are recession-resistant.

Growth: Where you will find companies with multiple growth vectors, able to surge during economic booms.

Both: Where you will find companies showing a balance between growth and stability.

Dividend Rock Stars List

The Rock Stars List is a selection of the safest dividend stocks.

The Rock Stars List is a selection of the safest dividend stocks.

Which dividend stocks are the best? Those with the highest yield? Or those with the strongest dividend growth?

Dividend Monk presents you with the Dividend Rock Stars list: a selection of companies showing income and growth. You guessed it; we prefer a combination of dividend growth and dividend yield. Let the list speak for itself.

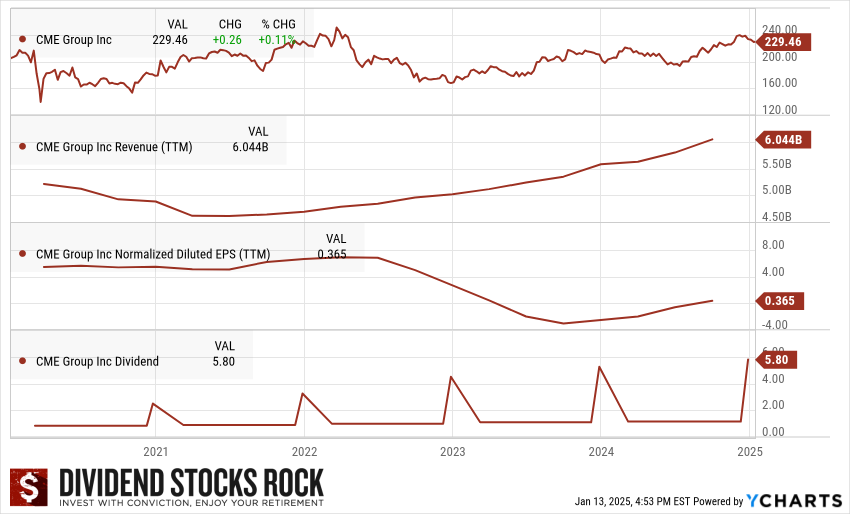

CME Group (CME)

Business model

CME Group provides a derivatives marketplace. The Company enables clients to trade futures, options, cash, and over-the-counter (OTC) markets, optimize portfolios, and analyze data. It exchanges offer a range of global benchmark products across all major asset classes based on interest rates, equity indexes, foreign exchange, energy, agricultural products and metals. It offers futures and options on futures trading through the CME Globex platform, fixed-income trading via BrokerTec, and foreign exchange trading on the EBS platform. In addition, it operates central counterparty clearing provider, CME Clearing. Its products provide a means for hedging, speculation, and asset allocation related to the risks associated with, among other things, interest rate-sensitive instruments and changes in the prices of agricultural, energy, and metal commodities. It provides clearing and settlement services for various exchange-traded futures and options on futures contracts and OTC derivatives.

Why we like it

CME Group is the dominant player in derivatives products. The need for hedging is on the rise as markets experience volatility. Options and futures are among the most used products in hedging strategies. The CME stock reached all-time highs after the sharp drop it experienced during the pandemic, but after a 2022 downturn, it returned to near-2020 levels. The good news is that the opportunistic time window for a potential buy seems now, even with the recent rally. Its special dividend increased by 30% with management’s commitment to give back to its shareholders.

This puts CME on the buy list for a long-term play. As the magnitude of rate cut expectations continues to fluctuate over the next 12 months, CME should benefit from interest rate volatility. Significantly, CME does not benefit from rising or falling interest rates; rather, it benefits when the path of rate movement is uncertain. Additionally, we believe CME’s fundamental improvement has not been appreciated. Shares of CME have traded relatively flat since 2019 despite margin expansion, 15%+ revenue growth, and 35%+ earnings growth.

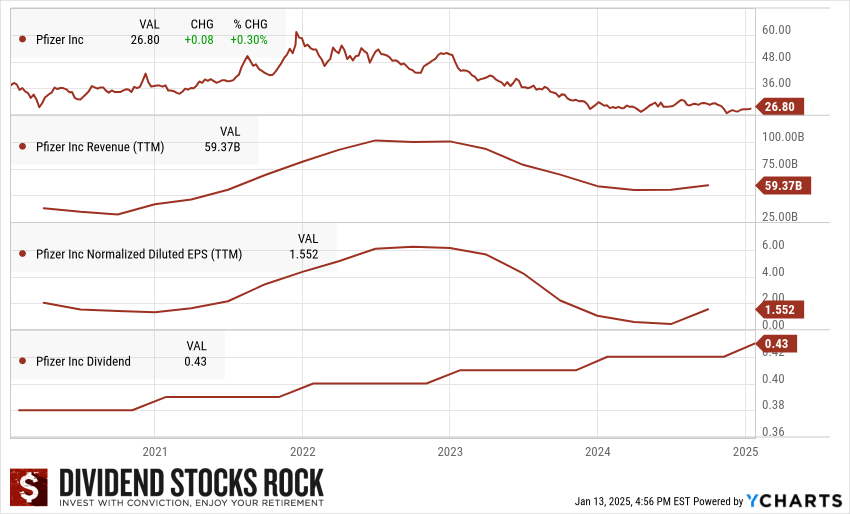

Pfizer (PFE)

Business model

Pfizer Inc. is a research-based global biopharmaceutical company. The Company is engaged in the discovery, development, manufacture, marketing, sale and distribution of biopharmaceutical products worldwide. Its Biopharma segment is involved in the science-based biopharmaceutical business. Its Biopharma segment includes the Pfizer Oncology Division, the Pfizer U.S. Commercial Division, and the Pfizer International Commercial Division. Its product categories include oncology, primary care and specialty care. Its Oncology products include Ibrance, Xtandi, Inlyta, Bosulif, Lorbrena, Braftovi, Mektovi, Padcev, Adcetris, Talzenna, Tukysa, Elrexfio and Tivdak. Its primary care products include Eliquis, Nurtec ODT/Vydura, Comirnaty, the Prevnar family, Abrysvo, FSME/IMMUN-TicoVac, Paxlovid and Lucira by Pfizer. Its specialty care products include Xeljanz, Enbrel (outside the U.S. and Canada), Inflectra, Cibinqo, Litfulo, Vyndaqel family, Genotropin, Sulperazon, Zavicefta, Medrol and Panzyga.

Why we like it

PFE faces a heavy patent expiration cycle but has built an impressive lineup of new drugs. In June 2019, PFE completed the acquisition of Array (ARRY) in an $11.4B deal. This addition will add several solid marketed drugs focusing on oncology and rare diseases. Thanks to its size and scale, PFE can develop and produce drugs more cheaply than many competitors. We see ongoing growth catalysts from several areas, including cardiology, immunology, and oncology. PFE divested its off-patent division at the end of 2020 (it became Viatris) to drive additional cash flow toward drug development and potential acquisitions. That’s what they did in 2023 with the announcement of the acquisition of cancer-focused big pharma Seagen for $43B. Pfizer believes Seagen could contribute more than $10B in revenues by 2030, with potential significant growth beyond that year. The market does not like the decision, and the stock price has declined ever since. Considering Pfizer’s historic business model and drug pipeline, it looks to be an interesting play in the healthcare industry.

Now that the company is done with the “COVID products sales drop,” Pfizer raised its 2024 revenue and adjusted EPS guidance, responding to sustained growth across its key therapeutic areas and anticipated upcoming product launches.

Dividend Rock Stars List

The Rock Stars List is a selection of the safest dividend stocks.

Which dividend stocks are the best? Those with the highest yield? Or those with the strongest dividend growth?

Dividend Monk presents you with the Dividend Rock Stars list: a selection of companies showing income and growth. You guessed it; we prefer a combination of dividend growth and dividend yield. Let the list speak for itself.

Leave a Reply