There’s a certain kind of business that doesn’t just sell products—it becomes part of the operating room, the recovery ward, and the hospital’s long-term strategy.

This one fits the bill.

As a leader in surgical technology, orthopedic implants, and advanced robotics, this healthcare company has turned precision and innovation into a wide economic moat. With thousands of patents, first-mover advantage in robotic-assisted surgery, and sticky supplier relationships, it’s quietly powering some of the most critical moments in modern medicine—and rewarding shareholders in the process.

Behind the Scalpel: The Tech Powering Long-Term Growth

Stryker (SYK) is a medical technology company that operates across two dominant segments:

-

MedSurg & Neurotechnology: This includes everything from surgical tools, endoscopy, and intensive care equipment to neurosurgical systems and emergency medical gear.

-

Orthopaedics: Known for its hip, knee, and shoulder implant systems, this segment includes tools and devices used in total joint replacement and trauma surgery. Its Mako surgical robot platform gives it a tech edge in robotic-assisted procedures.

With a product portfolio deeply embedded in hospitals and surgical centers, it enjoys a strong recurring revenue stream, particularly as providers move to consolidate suppliers and standardize care.

Tools, Trials, and the Truth: What Bulls and Bears See

Bull Case: Moats, Mako, and Momentum

Few companies in the medtech space offer this kind of vertical integration and brand loyalty. Surgeons often stick to what they know, and once a hospital adopts this platform, the switching costs are high—not just in dollars, but in retraining and surgical efficiency.

-

The company has a multi-year head start with its Mako surgical robots.

-

It has strong distribution and loyalty in orthopedic implants—a notoriously sticky market.

-

Hospitals want to consolidate suppliers, which directly influences their diversified product base.

Combined with innovation in AI-assisted care and remote monitoring, this stock blends surgical precision with long-term upside.

Bear Case: High Hopes and High Risks

Conversely, expectations for Mako are sky-high, and the competition isn’t standing still. Players like Zimmer Biomet and J&J are catching up with their own robotic platforms, and adoption depends on hospital budgets, not just technology.

Also, as with all medtech companies, there’s exposure to recall risks, regulatory hurdles, and legal liabilities, especially with the growing use of device registries. A single product flaw can become a multi-million-dollar headline.

Build a Portfolio That Pays You for Life

This kind of stock is what we look for: high-quality, future-focused, and still willing to send you a check every quarter.

But don’t stop at one.

If you’re serious about creating a reliable, rising income that can fuel your retirement (or just give you more financial freedom), then it’s time to grab our Dividend Income for Life Guide. It’s packed with the strategies and stock types we use to build portfolios that perform, with or without market drama.

Download your free guide here, and start building a portfolio that works hard for you.

What’s New? A Healthy Forecast Before Earnings Drop

Just ahead of its latest earnings release on May 1, analysts projected strong results:

-

EPS expected at $2.73 (+9.2% YoY)

-

Revenue estimated at $5.69B (+9.4% YoY)

If confirmed, this would mark continued momentum in both surgical technology and joint replacement—despite ongoing macro concerns like global trade tensions.

The company has continued to invest in innovation and operational efficiency, putting it in a strong position as healthcare spending rebounds.

Dividend Triangle in Action: Precision You Can Count On

Let’s break down how this stock performs across the Dividend Triangle:

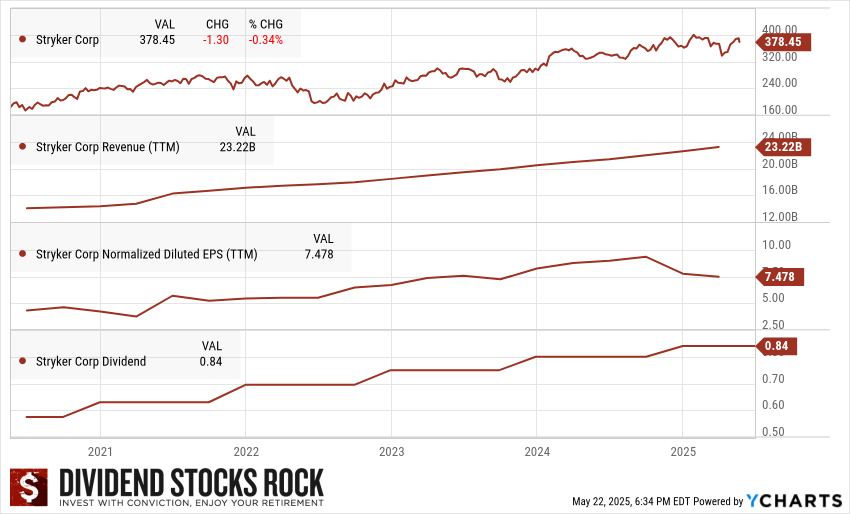

- Revenue: Now at $23.22B (TTM), revenue has climbed steadily every year. This shows strong adoption and cross-selling across its surgical, neuro, and orthopedic platforms.

- Earnings (EPS): Normalized EPS sits at $7.48 (TTM)—a solid upward trend, with occasional dips tied to R&D costs and integration expenses. Long-term, the earnings base remains strong and well-diversified.

- Dividend: The dividend has grown to $0.84/share, with a stable payout ratio and room to keep climbing. It’s not a high-yielder, but it’s a high-quality grower, backed by consistent cash flow.

Final Word: Innovation-Driven and Investor-Friendly

This medtech leader has created a rare blend of high-tech innovation and durable income.

It’s deeply embedded in hospital systems, holds strong pricing power through surgeon preference, and continues to invest in next-generation surgical and monitoring technology. With a growing dividend and proven resilience across healthcare cycles, it’s a name that fits right into a long-term income strategy.

Want a stock that’s quietly improving lives—and portfolios—one procedure at a time? This one’s got it stitched up.

Don’t Leave without Your Guide!

The Dividend Income for Life Guide shows you how to build a portfolio that generates reliable, growing income—without chasing yield or guessing the next hot stock.

It’s more than stock ideas; it’s about the right mindset to enjoy life and retirement without worrying about your income.

Download your free copy now and start creating income you can count on.