Let’s face it—this is a boring business. But if you’re looking for a company that keeps doing the job, year in and year out, this one deserves a spot on your radar.

It owns the rails. Literally. It moves over 300 million tons of goods across North America every year, and it gets paid whether the market’s up, down, or sideways.

You won’t get fireworks here, but you will get a rock-solid business with a rising dividend, backed by one of the most impenetrable moats in the market. This is the kind of stock that pays you to be patient—and rewards you for sticking around.

The Business Behind the Engine: How It Moves and Makes Money

Canadian National Railway (CNI) moves over 300 million tons of goods each year by rail and truck—linking ports, manufacturers, and distributors across the U.S. and Canada. It operates in four major areas:

-

Rail: The core of the business, supported by one of the best-positioned networks in North America.

-

Intermodal: Door-to-door solutions using containers and trucks, ideal for e-commerce and consumer goods.

-

Trucking: First- and last-mile transport, customs clearance, and cross-border freight.

-

Supply Chain Services: End-to-end logistics across multiple industries, including agriculture, chemicals, and autos.

The beauty here is diversification. When commodities like oil or lumber are down, segments like intermodal or autos help smooth the ride.

Bull and Bear Breakdown: Unshakeable Moat, but Limited Growth

Bull Case: Unshakeable Moat, Efficient Model, and a Dividend with Track Record

Let’s keep it simple—this business isn’t going anywhere.

You can’t build a competing railway today. The cost, the land, the regulation—it’s all prohibitive. That gives this company a near-impenetrable moat, backed by hard assets that keep generating returns.

It also has a strong history of operational excellence, with one of the best operating ratios in the industry (now down to 63.4%). That means it knows how to make more with less.

This isn’t a hyper-growth play—but it’s a long-term compounder. Buy it when it dips, collect the dividend, and watch the value roll in over time.

Oh—and it has raised its dividend consistently for over 25 years, showing it knows how to reward shareholders even when volumes fluctuate.

Bear Case: Expensive to Run, Limited to Grow

This business runs on steel and sweat—and both come with a price tag.

Railroads are capital-intensive. Tracks, trains, terminals—all require constant reinvestment just to maintain efficiency. And while management has done a great job keeping the operating ratio in check, rising maintenance costs are always a concern.

There’s also the issue of cyclical exposure. A downturn in commodities like grain, coal, or crude oil can quickly drag down volumes. When demand dries up, so does rail traffic.

Growth is another sticking point. After losing out on the Kansas City Southern acquisition, opportunities to expand the network are now few and far between. With limited M&A options, growth will likely come from efficiency, pricing, and volume recovery—not bold moves.

Want More Stocks like This One?

The Dividend Rock Star List was just updated—our monthly breakdown of the best dividend growers, screened and sorted so you don’t waste time chasing hype.

It’s packed with:

-

✅ Dividend growers with strong financials

-

✅ Reliable payers with long-term potential

-

✅ New opportunities we’re watching right now

Check out the freshly updated list here and see who’s making the cut this month.

What’s New? A Good Quarter Driven by Volume and Pricing Power

The company reported a strong Q1-2025:

-

Revenue up 4%

-

EPS up 8%

-

Operating ratio improved to 63.4%, showing continued efficiency

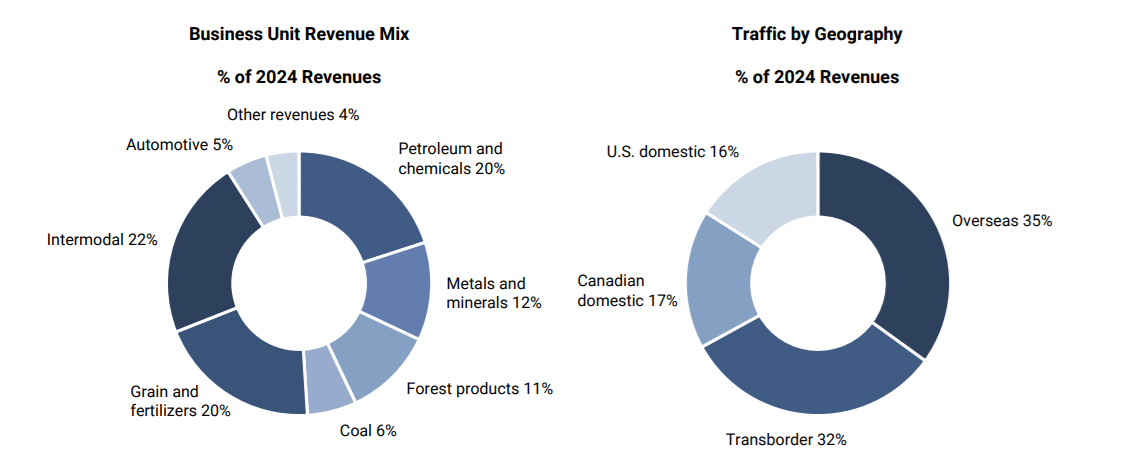

Growth came mostly from the grain & fertilizer (+11%), coal (+11%), and petroleum & chemicals (+7%) segments. While intermodal (-2%) and metals & minerals (-1%) softened a bit, freight revenue per ton-mile climbed—proving the company still has pricing power in this environment.

It wasn’t a blowout quarter, but it was exactly what you want from a company like this: steady, efficient, and shareholder-friendly.

Dividend Triangle in Action: Steady Tracs, Rising Payouts

Let’s break it down using our Dividend Triangle framework:

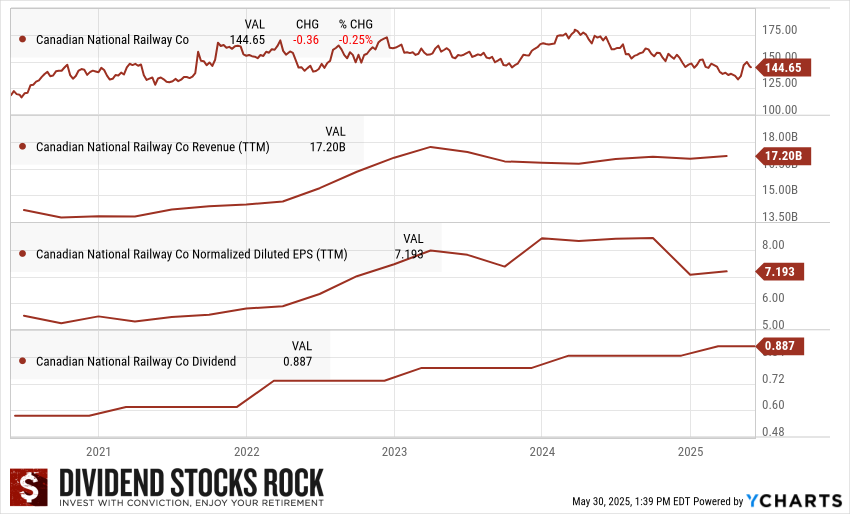

- Revenue: Now at $17.2B (TTM)—not flashy, but remarkably consistent, even through economic slowdowns.

- Earnings (EPS): EPS sits at $7.19 (TTM), reflecting smart cost management and margin stability. It’s bounced back quickly from earlier dips.

- Dividend: Currently at $0.887/share, the dividend continues its climb. This stock has increased its dividend every year for more than 25 years—a quiet but powerful signal of strength.

Final Word: Built Like a Locomotive and Pays Like One, Too

This is one of those stocks you buy when it dips and never worry about.

It runs on a near-impossible-to-replicate network, manages costs better than most, and touches every corner of the North American economy. It’s not exciting, but it’s exactly the kind of dividend growth stock that quietly compounds in the background while the rest of the market fights for attention.

Add in a 25+ year dividend growth streak, a strong balance sheet, and pricing power in multiple segments, and you’ve got something rare: a stock that doesn’t need headlines to deliver long-term value.

When you’re building for income, consistency wins. And this one’s been showing up for decades.

Updated Monthly, Built for Long-Term Income

This stock made the cut—and so did many more.

The Dividend Rock Star List is your shortcut to finding real dividend growers—the ones that don’t just pay, but grow and protect your income through every cycle.

Grab the latest version here—we just updated it, and we do it every single month.