For all drug manufacturers (major, generic or specialty), biotech, diagnostics, and research companies, most of their budgets go towards Research & Development. They must manage their pipeline of new products and their patents. A company may be able to surf on its previous successes for a decade due to their patents’ protection of their research. However, they must constantly renew their portfolios. This frequently impacts their ability to increase their dividends in a predictable manner. Price volatility both up and down are also frequent characteristics of companies in this industry.

As for Healthcare plans, long-term care facilities, medical care and distribution companies are more likely to be affected by governmental regulations. The cost of healthcare is a major topic for governments across the world. Should it be free, sponsored or insured? This question leads to much debate and uncertainty for the future. No matter what happens, the industry will find a way to adjust their business models, but volatility will be the continuing and on-going characteristic of this sector.

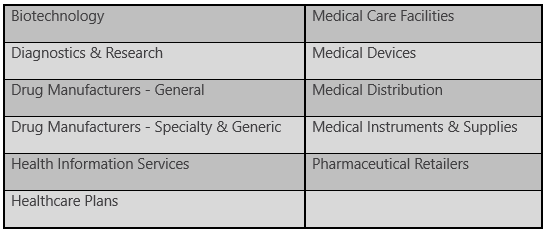

Sub-Sectors (Industries)

Greatest Strengths

The advantage for dividend investors in this sector is the wide choice of large and well-established companies. The best performing companies in this sector are often the long-term established companies that have a strong distribution network or a large drug portfolio and pipelines full of new products. Big pharmaceuticals usually offer a safe haven for your money over the long run. They know how to manage their R&D budgets and drug pipelines. The healthcare sector often sees stock surges both upward and downward based upon the results of their discoveries. Patents and regulations are part of their daily routine.

Medical devices, instruments or supply companies will provide products with repetitive purchases. They enjoy wide distribution networks, loyal customers, and constant repeat orders. They can make great dividend growers too.

Greatest Weaknesses

Unfortunately, as R&D budgets are often a huge part of a healthcare company’s expenses, there are many companies showing an erratic dividend growth track record. It is not that they will cut their dividend, but you may be waiting for a few years before seeing a dividend increase.

When you consider healthcare plan and medical distribution industries, they face harsh competition and must operate in a razor-thin margin environment. If they make one bad acquisition or hit a speed bump, such companies will see cash flow evaporate quickly. There are currently many changes in the air around healthcare regulations. There is a political will to make healthcare more affordable. This could have an impact on those industries.

Finally, Medical care facilities have had their fair share of problems in the past. With the pandemic, it has become quite a challenge to manage raising expenses (to make sure both employees and seniors are safe) and weaker occupancy rates. Proceed with caution.

How to Get The Best of It

Big pharmaceuticals will often come with massive stock price fluctuations. A patent expiring, news about a new drug or a major acquisition could contribute to Mr. Market’s mood swing. These situations give you your chance to pick a solid dividend grower at a rebated price. I picked up shares of Johnson & Johnson (JNJ) during their quality control issues back in 2012-2013 and benefited greatly from that move.

In general, the healthcare industry is capital-intensive or requires a significant size to perform efficiently. Make sure the debt burden on your chosen company is not too large to manage efficiently. For distribution and healthcare plans, take a close look at their margins over time.

The healthcare sector is usually ignored during bull markets. There are more exciting companies to buy and this translates into a good buying opportunity. Most importantly, you must be patient with healthcare businesses. It may take time before the market realizes the value inherent in a particular company’s stock.

The healthcare sector is best for income investors.

Favorite Picks

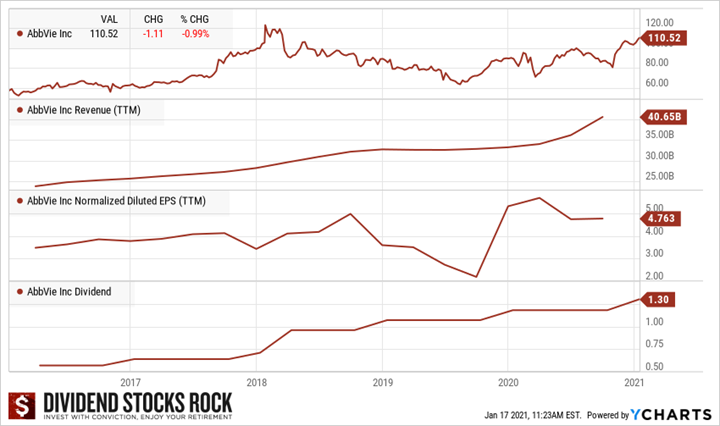

AbbVie (ABBV)

- Market cap: 188B

- Yield: 5.00%

Business Model

AbbVie is a drug company with strong exposure to the immunology and the oncology markets. The company’s top drug, Humira, represents over half of the company’s current profits. As the Humira patent expiration is imminent, the company is counting on other drugs such as Imbruvica and Venclexta to become more important growth vectors. The company was spun off from Abbott in early 2013. The recent announced acquisition of Allergan will add several new drugs in aesthetics and women’s health. It will also add a legal department with a strong expertise in patents and trademarks.

Investment Thesis

ABBV’s strength resides in Humira, a tumor necrosis factor blocker that reduces the effects of an inflammatory body substance. Humira is about 50% of ABBV sales and even more of its profit. The company is currently enjoying the last few years of Humira’s various patents across the world. New immunology drugs such as Skyrizi and Rinvoq could replace a good part of Humira’s sales slowdown. ABBV’s growth also lies in its new cancer drug, Imbruvica. We also see promising growth from its psoriasis and rheumatoid arthritis drugs. The idea behind buying Allergan was primarily to diversify ABBV revenue sources and find cleverer ways to extend its patents. AGN’s, like ABBV’s, legal department is known for its “creativity.” Issuing a trademark for Botox was very smart. The recent dividend increase confirms our bullish thesis.

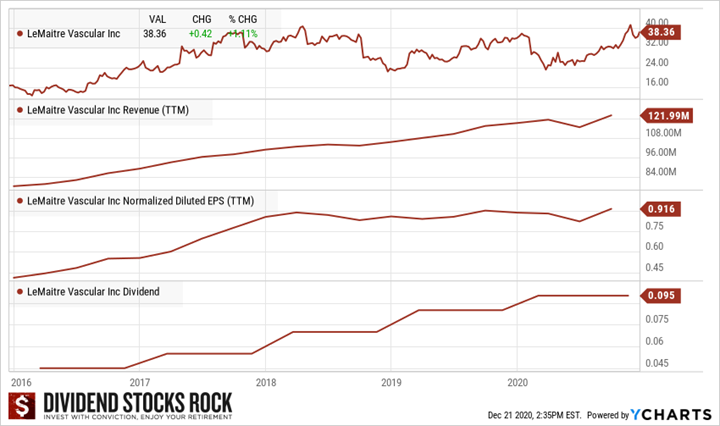

LeMaitre Vascular (LMAT)

- Market cap: 188B

- Yield: 0.80%

Business Model

LeMaitre Vascular Inc. manufactures and distributes medical devices for the treatment of peripheral vascular disease. Its products are primarily used during open vascular surgery and address several anatomical areas, such as the carotid, lower extremities, upper extremities, and aorta. The firm’s lower extremities product line contributes the largest proportion of revenue, followed by the carotid line. LeMaitre’s surgical devices include angioscopes, balloon catheters, carotid shunts, phlebectomy devices, vascular grafts, vascular patches, and vessel closure systems. LeMaitre generates most of its revenue in the United States. Sales in Germany also contribute a significant proportion of total revenue.

Investment Thesis

When we look at LeMaitre Vascular, the first word that comes to our mind is “growth”. The company shows strong revenue growth as it has acquired 24 businesses over the past 23 years. LMAT also counts on a solid salesforce and engineering department to sell and develop new products. The company currently offers over a dozen products being used in surgeries on veins and arteries outside of the heart. The pandemic has caused a slowdown this growth vector (going from 110 to 79 sales rep this year), but you can expect more representatives in 2021-2022 as the vaccines are distributed across the world and surgery events increase.