The basic materials sector will include most natural resources used to make goods. This sector includes companies involved in the discovery, development, and processing of raw materials. This includes various metals (copper, gold, silver, etc.), agricultural inputs like fertilizers, lumber & wood (along with paper products) and specialty chemicals.

Sub-Sectors (Industries)

Greatest Strengths

If you know a specific industry inside out (the needs and trends for copper for example), you can make a lot of money. Basic materials companies’ financial health will vary following the demand vs supply cycle. This is a sector prone to show many significant stock price movements within a comparatively short period of time. If you can buy industry leaders at their bottoms, you will look like a genius in the next commodity boom.

Some companies in the chemical and specialty chemical industries offer products that will be bought no matter what is happening in the economy. Such companies that produce those stable products enjoy stronger pricing power, are less dependent on commodity prices, and could become good dividend growers.

On another topic, gold is often seen as an asset class of its own. Throughout most recessions, gold (the metal) and gold companies (mining or royalties) have done very well. In general, when the market goes into full panic mode, many investors seek a place to store their money. They don’t necessarily trust currencies (or governments) and believe gold is a more reliable currency. Therefore, if you hold gold stocks, you will likely see them doing nothing for several years, but they will look like saviors when there is panic in the streets. In my view, gold is a bet on fear. Over the long haul, its returns have matched inflation.

Greatest Weaknesses

The basic materials sector is relatively small when you only consider dividend paying companies. This is explained by the highly cyclical and volatile nature of the sector. The price of many commodities fluctuates a great deal, and it makes it difficult for management to plan steady and increasing dividend payouts.

In addition to their cyclical nature, most basic materials require significant amounts of capital to operate. This often leaves little room for dividend growth, particularly during economic downturns. This is also why these companies are likely to cut their dividend temporarily to assist the business in weathering challenging times. Management’s goal is not to fill shareholders’ pockets with distributions, but rather to improve their production abilities and lower their costs of operations.

How to Get The Best of It

Trends! If you were a DSR member, you’d already know that I’m not a big fan of either the basic materials or the energy sectors. They make for poor dividend growers due to their dependence on commodity prices. However, if you want to make speculative plays, this is one of the best sectors to play in. Whenever there is a bottom, you can aim at picking some leaders in the industry (look at their balance sheet and ability to generate cash flow) and you can make great trades. Still, you will not see me being overly hyped about any basic materials companies.

The basic materials sector is best for growth investors.

Webinar: Where to Invest in 2021?

2,000+ investors saw this webinar already.

- KM: “Amazing webinar! Thanks very much!”

- Cheryl: “With thanks, I’m impressed!”

- Harley: “Thank you for your passion Mike.”

- Roberta: “I’m such a huge fan of DSR! Well done, Mike.”

Favorite Picks

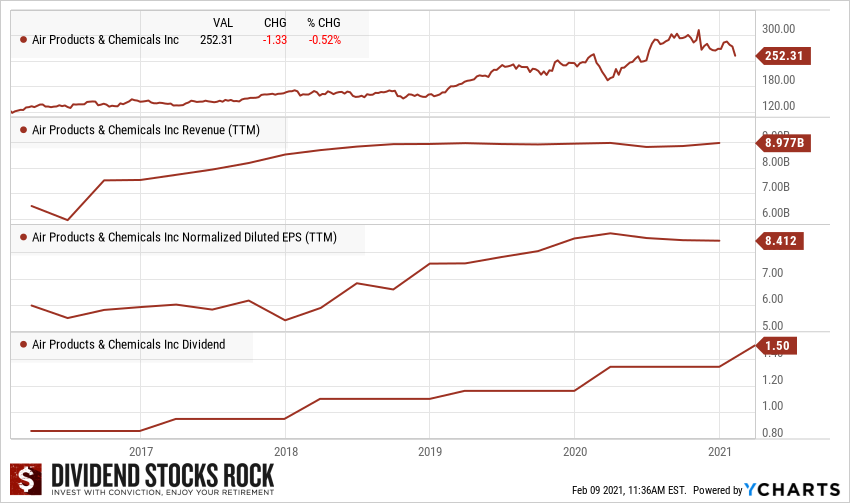

Air Products & Chemicals (APD)

- Market cap: 61B

- Yield: 1.95%

- Revenue growth (5yr, annualized): 2.51%

- EPS growth rate (5yr, annualized): 7.62%

- Dividend growth rate (5yr, annualized): 10.11%

Business Model

Since its founding in 1940, Air Products has become one of the leading industrial gas suppliers globally, with operations in 50 countries and 19,000 employees. The company is the largest supplier of hydrogen and helium in the world. It has a unique portfolio serving customers in several industries, including chemicals, energy, healthcare, metals, and electronics. Air Products generated $8.9 billion in revenue in fiscal 2020.

Investment Thesis

APD has found an interesting way to position its business in a sector where most are stuck with commodity price fluctuations. By providing industrial gases, APD signs long-term contracts with its customers. Industrial customers are more interested in stability and reliability than costs since gases are a small part of their expenses but are vital for their business. ADP has made a smart move in acquiring Shell’s and GE’s gasification businesses in 2018. The company became a leader in this field and has opened doors to expand its business in China and India. Finally, APD as an ambitious growth plan in motion including total capital expenditure of $18B. Those investments should support APD’s internal growth for the decade to come.

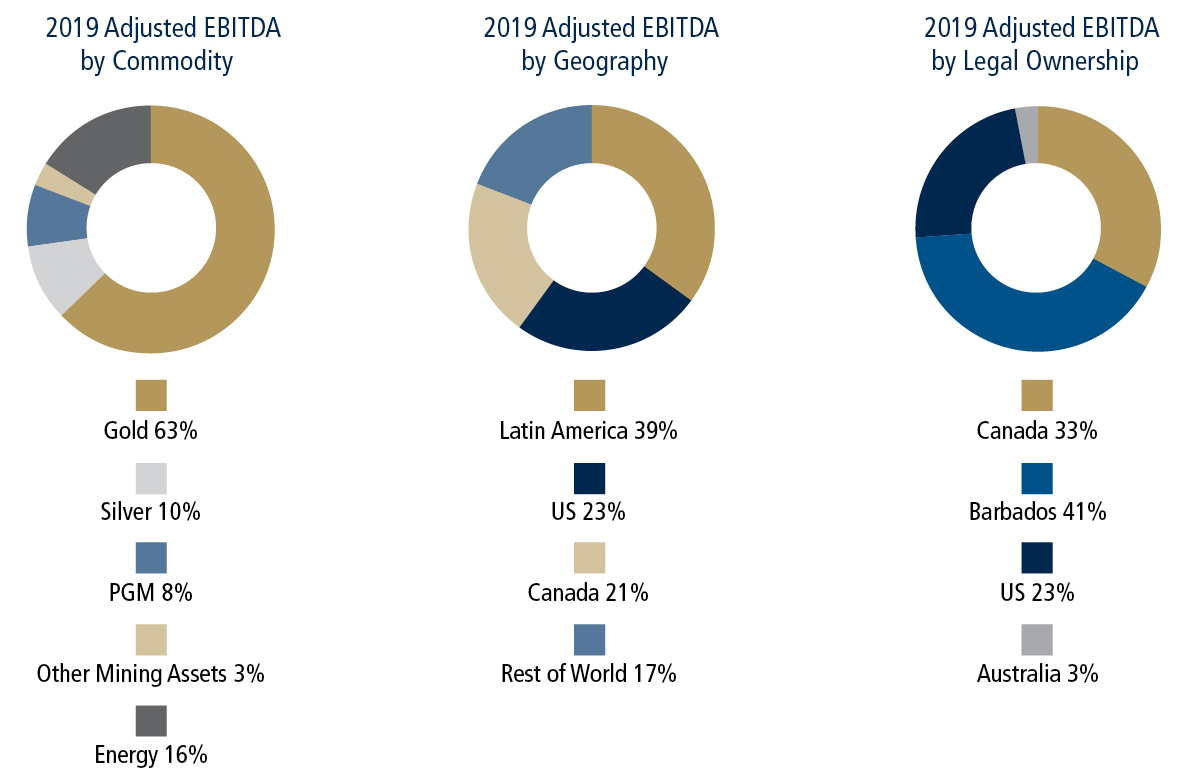

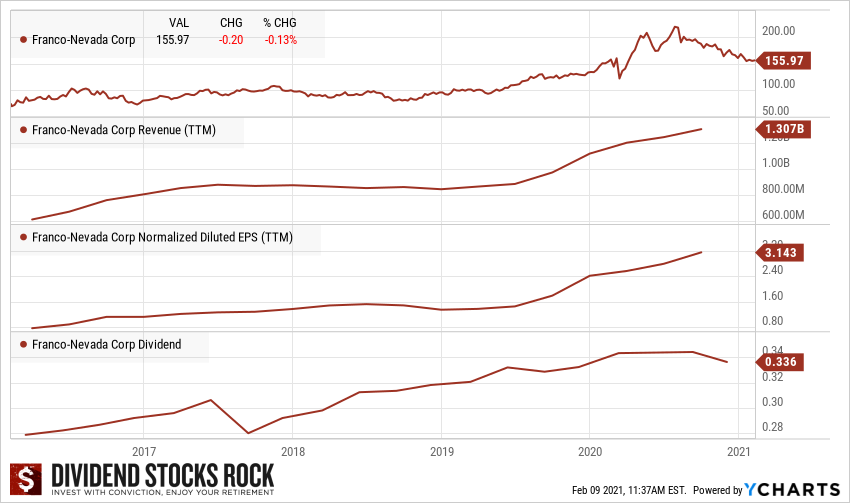

Franco-Nevada Corp (FNV) (FNV.TO)

- Market cap: 30B

- Yield: 0.66%

- Revenue growth (5yr, annualized): 18.05%

- EPS growth rate (5yr, annualized): 25.73%

- Dividend growth rate (5yr, annualized): 10.57%

Business Model

Franco-Nevada Corp is a royalty and investment company focused on precious metals. The company owns a diversified portfolio of precious metals and royalty streams, which is actively managed to generate the bulk of its revenue from gold, silver, and platinum. The company does not operate mines, develop projects, or conduct exploration. Franco-Nevada’s short-term financial performance is linked to the price of commodities and the amount of production from its portfolio of producing assets. Its long-term performance is affected by the availability of exploration and development capital. The company holds a portfolio of assets, diversified by commodity, revenue type, and stage of a project, primarily located in the U.S., Canada, and Australia.

Investment Thesis

Franco-Nevada doesn’t waste its time operating mines, but rather manages a portfolio of royalty streams. The company owns 45,300 square kilometers of geologically prospective land but will let “gold miners” spend the time and money on exploration. If the miners find something, the royalty will kick in. We like this “cash flow focused” business model. As FNV is a play on gold and precious metals, it enjoys stronger cash flows when gold prices surge. The company shows unparalleled portfolio diversification offering shareholders some peace of mind in volatile markets. It is a “Covid-19” proof business model.