Each month, we issue The Mike’s Buy List for our DSR members. They get our best ideas for both U.S. and Canadian dividend stocks. The first Friday of each month, they receive our top 10 growth and top 10 retirement (yield over 4%+) investment ideas.

Today, we’ll discuss two ideas among the list: ViacomCBS (VIAC) and AbbVie (ABBV).

Growth Perspective: ViacomCBS (VIAC)

Business Model

ViacomCBS is the combination of CBS and Viacom that has created a media conglomerate operating around the world. CBS’ television assets include the CBS television network, 28 local TV stations, and 50% of CW, a joint venture between CBS and Time Warner. The company also owns Showtime and Simon & Schuster. Viacom owns several leading cable network properties, including Nickelodeon, MTV, BET, Comedy Central, VH1, CMT, and Paramount. Viacom has also built several online properties on the strength of these brands. Viacom’s Paramount Pictures produces original motion pictures and owns a library of 2,500 films.

What’s the Story

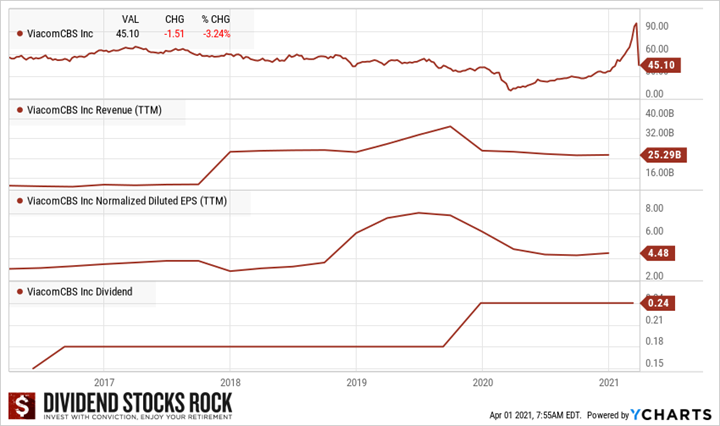

Not long ago, the stock lost 50% of its value in 5 days. That’s crazy, right? It all started when VIAC announced an equity issue in new Class B common shares and mandatory convertible preferred shares. The arrival of 20 million new shares was the first spark to a significant sell-off. We think it was a smart way to cash in on a high valuation to support spending on its new streaming business. The company’s future is tied to its ability to generate content and attract customers on its streaming platforms.

Then, the stock continued to drop as Archegos Capital (a hedge fund) was forced to sell more than $20B in stocks on Friday due to a margin call. VIAC lost 50% of its value in a single week. It’s an interesting speculative play but proceed with caution. The company shows a dividend safety score of 2 since it increased its payout only once in the past 5 years. However, the dividend is safe with low payout ratios. Management prefers to focus on growth (the integration of the merger + massive CAPEX toward streaming), which is not necessarily bad. After this stock price drop, the company now trades at a PE of 12. Not bad in an “overvalued market” and worth a look at this time.

Investment Thesis

The merger between both companies was a good idea. Content creation is expensive (the company spends $3B per year on this) and limits new players to enter this playground. VIAC now enjoys a strong broadcast network reaching over 100M American households. The company offers popular and unique channels and sports broadcast rights to advertisers. It used to license its content to other streamers like Netflix, but this may change in the future as VIAC is working on combining Paramount and CBS All Access together in its own streaming service. Are they late to the dance? Will advertisers come back in strengths after the economic lockdown? How are the merger synergies coming along? There are lots of uncertainties around VIAC (do your own due diligence), but we think it shows great potential.

Potential Risks

First, CBS and Viacom picked an inopportune time to consume their merger. As they are in the middle of their integration, the pandemic is forcing people to stay home. While TV watching time surges, advertising budgets have plummeted. Many industries have no reason to advertise during the lockdown (movies, fast foods, autos, etc.). If the covid-19 outbreak does not come under control, major sports events will remain uncertain. This will affect VIAC’s bottom line at a time where it just borrowed substantive funds for the merger in 2019. The company may be entering the streaming service party a little late. It was licensing its content before, but now it seems like they want to become another player in this growing industry.

Retirement Perspective: AbbVie (ABBV)

Business Model

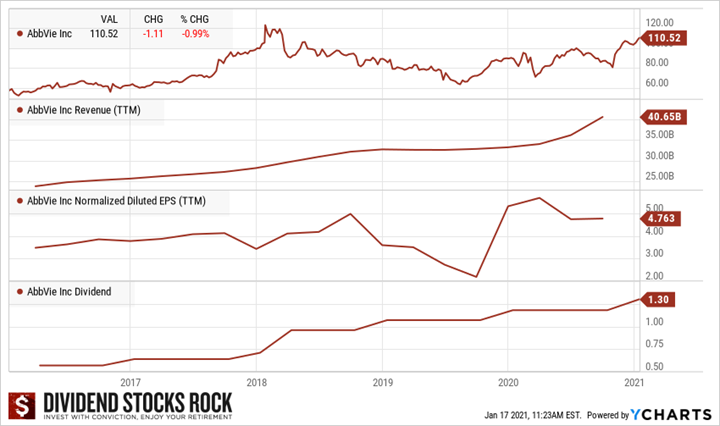

AbbVie is a drug company with strong exposure to the immunology and oncology markets. The company’s top drug, Humira, represents over half of the company’s current profits. As the Humira patent expiration is imminent, the company is counting on other drugs such as Imbruvica and Venclexta to become more important growth vectors. The company was spun off from Abbott in early 2013. The recently announced acquisition of Allergan will add several new drugs in aesthetics and women’s health. It will also add a legal department with strong expertise in patents and trademarks.

What’s the Story

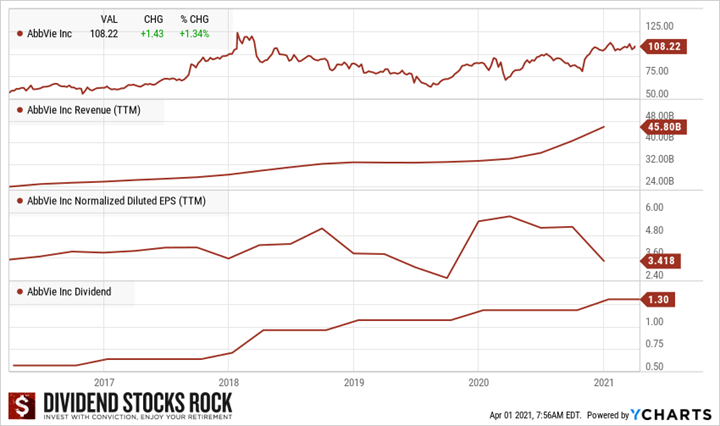

There was not much to report this month on AbbVie. Sometimes being a dividend growth investor isn’t that exciting!

On March 30th, the FDA accepted AbbVie’s new drug application for Atogepant. The application targets the preventive treatment of migraine headaches.

According to Reuters, ABBV is in discussions to sell a $5B portfolio of women’s drugs it acquired last year through its purchase of Allergan. AbbVie is working with Morgan Stanley on an auction process that has attracted interest from private equity firms including CVC Capital Partners, according to the article.

Investment Thesis

ABBV’s strength resides in Humira, a tumor necrosis factor blocker that reduces the effects of an inflammatory body substance. Humira is about 50% of ABBV sales and even more of its profit. The company is currently enjoying the last few years of Humira’s various patents across the world. New immunology drugs such as Skyrizi and Rinvoq could replace a good part of Humira’s sales slowdown. ABBV’s growth also lies in its new cancer drug, Imbruvica. We also see promising growth from its psoriasis and rheumatoid arthritis drugs. The idea behind buying Allergan was primarily to diversify ABBV revenue sources and find cleverer ways to extend its patents. AGN’s, like ABBV’s, the legal department is known for its “creativity.” Issuing a trademark for Botox was very smart. The recent dividend increase confirms our bullish thesis.

Potential Risks

As the drama about Humira’s patent expiration (2023 for the U.S.) shows us, the drug industry is all about patents and competition. Why? Because it allows the winner to reap the benefits of billions invested in R&D. Therefore, ABBV must deal with competitors’ drugs not related to patents. While ABBV might be one discovery away from making billions, the same goes for about any competitor. For instance, Pfizer could deteriorate ABBV sales expectations. Now, ABBV must convince the market its pipeline is worthy of its investment. A few more quarters should be necessary. ABBV is increasing its leverage through the acquisition of Allergan. Both Humira from AbbVie and Botox from Allergan are star products that could face heavy competition going forward and hurt the ABBV bottom line.

Take Some Time to Rate Before Buying!

I believe every investor should have all of its stocks ranked. Rating your holdings according to a simple, but an efficient set of metrics will also solve your buy & sell dilemma. You will automatically identify the strong companies and weak companies in your portfolio. I’ve discussed my ranking system on my YouTube channel.