Ah, forever stocks! I love them. Here I present nine stocks I include in my U.S. forever stock selection, and briefly explain why. A forever stock is one I’d buy for the long haul, 10+ years. It offers reliable growth and is so solid and resilient that I can forget about it and sleep soundly.

Let’s be clear, my selections aren’t based on timing; I’m not saying that they are great buys right now, but rather that I’d buy any of them and, if I couldn’t monitor them quarterly as I do, I wouldn’t worry.

Sleep-well-at-night forever stocks share several of these qualities:

Diversification

Diversification- Market leaders

- Economies of scale

- Predictable cash flow

- Stable and/or sticky business model

- Essential products / services

- Multiple growth vectors

- Long dividend growth history

This list is partial; clearly, there are other contenders that could be on it.

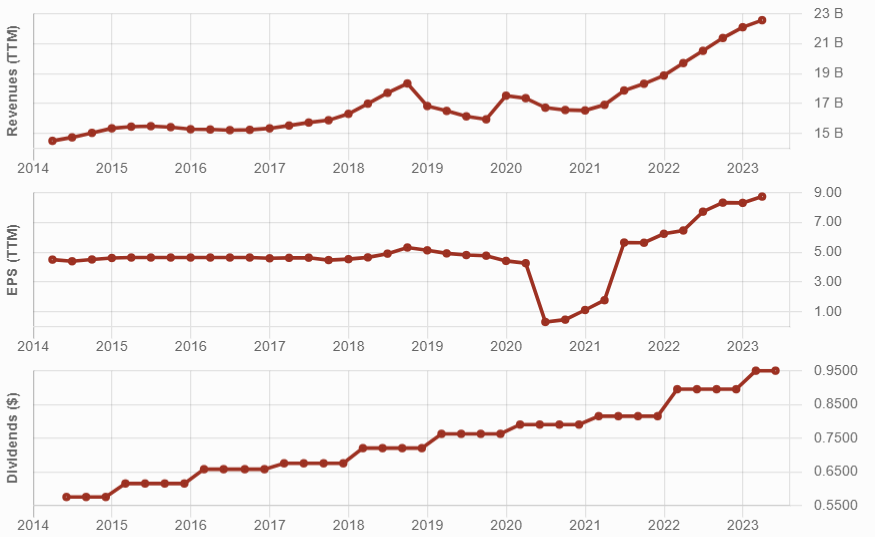

Procter & Gamble (PG) – Consumer Staples

Procter & Gamble has learned from its mistakes and manages one of the largest portfolios of billionaire brands. Buying PG shares is like buying an ETF of consumer staples. Its focus on brand management, keeping only the most profitable and promising brands, is a key factor in choosing PG.

PG sells everything everywhere. It comes through any recession or crisis as its economies of scale help its margins and its iconic brands remain in the minds of billions of consumers.

A great example of their brand portfolio strength was how it increased its prices over the past 18 months to fight inflation. Once again PG showed its strong pricing power and how it can maintain healthy margins.

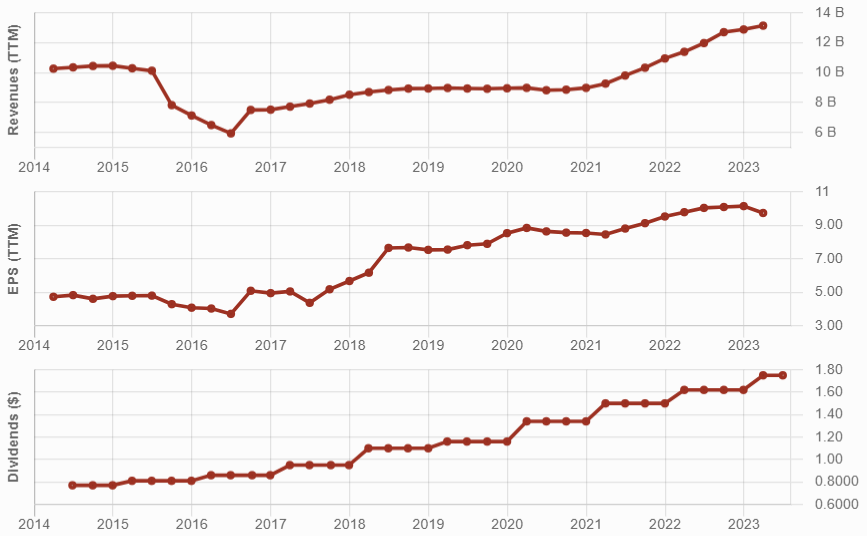

Genuine Parts (GPC) – Consumer Discretionary

GPC’s longevity is beyond other companies in this sector, with dividend increases every year since 1957! The secret behind 66 consecutive pay raises? Repeated necessary purchases.

GPC offers a wide variety of replacement automotive and industrial parts. While Magna sells parts to auto makers, GPC helps its customers to repair what they already own. With its economies of scale, GPC has become an uncontested market leader. It’s slowly but surely adding growth via small acquisitions to ensure it remains on top. GPC is a dividend king and replacement parts king!

BlackRock (BLK) – Financials

BlackRock is the world largest asset manager, with money invested in literally everything, and the largest ETF manufacturer. BLK’s business is very sticky since a lot of its revenue comes from institutional investors. BlackRock has become a must have for many investing strategies. There’s a lot of growth to grab in the wealth management market!

Patience is required with asset managers in an uncertain market. It’s all about charging fees on assets under management. When the market drops, asset managers generate less money. Also, many income-seeking investors are going back to fixed income and GICs. Let’s just say the margin is a bit less on such products than on emerging market funds!

Johnson & Johnson (JNJ) – Healthcare

JNJ is one of the first dividend growers I bought over 10 years ago. I even forget I have JNJ in my portfolio! It’s a “sleep well at night” stock. Today, JNJ shows a total return above 250%, including dividends, it’ll be in my “triple digit club” for at least another decade!

JNJ is one of the largest companies in healthcare, with strong economies of scale. It specializes in specialty drugs that are hard to replicate; its products have longevity. More income leads to more R&D investments; a virtuous circle where more money in R&D leads to a stronger pipeline, which leads to more sales. I love JNJ as a core holding!

For more great stock ideas, download our Rock Starts list, updated monthly!

A O Smith (AOS) – Industrials

Unusually, I picked a stock that I don’t own. A O Smith provides essential products like water treatment solutions. The leader in North America, AOS is expanding in the rest of the world. Robust demand for water treatment will continue to grow as water gets rarer. China, India, and other water treatment segments represent 36% of sales and the company’s fastest-growing opportunities. For investors wanting to dip their toe in water needs, AOS has a proven business model and it’s a dividend aristocrat.

Apple (AAPL) – Information Technology

Apple has a unique way to generate cash flow. It built an ecosystem of successful products that hasn’t been replicated so far. All devices communicate and connect seamlessly creating an obstacle for customers wishing to switch from iPhone to Google Pixel for example.

Apple doesn’t make products, but iconic artifacts to raving fans. AAPL doesn’t need to be the first mover to get the advantage on the market. With abundant cash flow generation, it waits, observing how a new market develops. Then, it moves into development at full strength and improves on what is already there. A great example is the Apple Watch. Where many failed, Apple built a billion-dollar business on people’s wrists!

Air Products & Chemicals (APD) – Materials

APD is the world’s largest supplier of hydrogen and helium, with facilities located on customer sites. These industrial gases aren’t a big part of their customers expenses but are crucial for their operations. This very sticky business model, where customers won’t expel APD from their operational sites, generates predictable cash flows and 40 consecutive years of dividend increases. APD’s business model is very hard to replicate, ensuring a great future.

I added APD to my retirement account (not displayed at DSR) earlier in 2023. It was on my wish list for a while!

Equinix (EQIX) – Real Estate

Equinix is the leader in a growing industry, data centers. Sure, you could fill an RV with servers, to create your own mobile data center. EQIX goes a lot further than that. This REIT is known for its co-location services. What does that mean? Many companies share the costs of a data center, like roommates splitting the rent.

Companies reduce their risk by dealing with EQIX. Its redundancy is far more reliable that any in-house system and provides better response times for companies who do business together and from the same data center. Its cloud-based global platform, through a distributed infrastructure, is a critical source of differentiation. With over 10,000 customers, including 1,800 networks, EQIX is a well-diversified cash cow.

EQIX is the largest REIT in this industry and is diversified across the world. The need for data centers will continue to explode in the coming years. For more about EQIX, see this recent article.

American Water Works (AWK) – Utilities

Something universal, water distribution. The investment thesis for American Water Works (AWK) is simple: an investor is buying shares of a monopoly selling an essential product with repeat purchases. As population grows, water needs increase, and the company operates a near recession-proof business. The yield (2%) and PE ratio don’t make it appealing, but if you’re looking for a safe place to park money for the 10 years, water is a pretty smart play.